はじめに 世界的なエネルギー需要の増大に伴い 中長期的なエネルギー需給の逼迫 不安定化や 化石燃料の消費による二酸化炭素排出量の増加がもたらす地球温暖化が懸念されている 省エネルギー 再生可能エネルギー導入等 ( 以下 省エネルギー等 という ) はこれを解決する有力な手段として 世界各国が協力して

|

|

|

- ありさ ひめい

- 6 years ago

- Views:

Transcription

1 平成 26 年度国際エネルギー使用合理化等対策事業 インドにおける運輸部門に係る省エネルギー等政策共同研究事業 報告書 平成 27 年 2 月 一般財団法人日本エネルギー経済研究所

2 はじめに 世界的なエネルギー需要の増大に伴い 中長期的なエネルギー需給の逼迫 不安定化や 化石燃料の消費による二酸化炭素排出量の増加がもたらす地球温暖化が懸念されている 省エネルギー 再生可能エネルギー導入等 ( 以下 省エネルギー等 という ) はこれを解決する有力な手段として 世界各国が協力して推進する必要がある 日本は世界でも有数の先進的な省エネルギー等技術やそれら技術を育んだ政策 制度等のノウハウを有しており 世界的な省エネルギー等の推進のため 率先して国際的イニシアティブを発揮することが期待されている インドにおいては 省エネルギー及び環境保全対策を進める余地 必要性が大きい 他方 同国では 現在 運輸部門で消費される燃料価格を政府が決定しており 自動車用燃料価格は政策的に低く抑えられている このような燃料価格政策をもって 運輸部門の省エネルギー等の推進 環境保全対策が阻害されていると考えられる 加えて 現在の補助制度の原資は 政府による石油債権の発行及び国営石油会社による負担で成り立っているが 昨今の原油価格の高止まりや燃料需要の増加によって 将来的に補助制度による財政への影響が拡大することが見込まれる こうした補助制度に用いられている政府資金を 省エネルギー等の促進に振り替えることは インド国内のみならず世界規模でのエネルギー需給安定化の観点から 極めて有益である 2013 年 9 月の日印エネルギー対話においては 自動車に限らず運輸部門において 同対話の下に設置された省エネルギー作業部会や各種調査事業を通じて 日印関係者間で定期的に情報共有及び意見交換を行うとともに 優れた省エネ技術を普及させていく上での課題及びその解決策を議論することが合意されている このような背景を踏まえ 本調査においては 運輸部門における省エネルギーの普及び促進事業及びエネルギー政策についての共同研究を実施し 当該国における今後の省エネルギー等の推進に資するエネルギー政策の在り方等に関する政策を提言することを通じて 世界のエネルギー需給バランスの安定化やエネルギー効率の大幅な改善に資することを目的とする 2015 年 2 月一般財団法人日本エネルギー経済研究所 1

3 目次 1. インド運輸部門 概況 運輸需要 エネルギー消費量 運輸部門の燃料補助政策及び省エネ政策動向 燃料補助金 燃費基準 排出基準 インド運輸部門の課題 グジャラート州における燃料消費実態と省エネ行動に関するアンケート調査 概要 目的 方法 分析結果 アンケート対象者の属性 二輪及び乗用車の保有 利用状況 乗用車の購入段階における燃費選好 燃料価格の変動による行動変化 公共交通の利用 政策への示唆 モデル分析 シナリオ分析の枠組み シナリオ分析の主要結果 BAU ケース シナリオの主要結果 シナリオ別乗用車エネルギー需要見通し比較 政策への示唆 鉄道 概況 所管官庁及び関連企業 インド国鉄の概要 インド国鉄の省エネ等の取組 新政権の鉄道政策

4 貨物 旅客 遠隔地 北東部及びアンドラ プラデシュ州とテランガーナ州の開発 鉄道部門の政策課題 国鉄運営 省エネルギーに関する課題 PAT 制度の可能性 (Perform, Achieve and Trade) ワークショップ開催概要 政策提言 今後の課題 Appendix 1 アンケート質問票 Appendix 2 アンケート結果 参考文献

5 1. インド運輸部門 1.1. 概況経済成長が続くインドでは 旅客 運送需要が増加し続けており ガソリンや軽油などエネルギー消費量が増大している 図 1-1 に示すように インド経済は 1980 年代から平均 6% 程度で成長してきた 1991 年に経済成長率が一時的に 1% 以下の水準に落ち込んだが その後は平均 6% 程度を保っている 直近では 2010 年に初めて 10% 台の経済成長を達成したが 2012 年 2013 年は経済成長が足踏みしている 一人当たり実質 GDP は右肩上がりに上昇を続け 自動車の登録台数も増加し続けている 図 1-2 は 実質一人当たり実質 GDP と自動車登録台数の推移である 1961 年の一人当たり実質 GDP が 2,000 ドル台後半 総自動車登録台数が約 66 万台であった その後 2012 年には一人当たり実質 GDP は 10,000 ドルを超え 総自動車登録台数も 1 億 6,000 万台まで増加した このうち 総自動車登録台数の大半は二輪車である 図 1-3 に示すように 二輪車の登録台数が最も大きな割合を占め 直近では 1 億 1,500 万台が登録されている 乗用車について 図 1-4 に示すように SIAM(Society of Indian Automobile Manufacturers) の販売統計では 2012 年に 267 万台の自動車販売されており これは 2005 年比で 2.6 倍の水準にまで増加したことがわかる 一方で 乗用車の保有水準は 他の途上国と比較して低い水準にある 図 1-5 は 千人当たり自動車保有台数の比較である タイ インドネシア 中国と比較して インドの千人当たり自動車保有台数は 17 台 / 千人である GDP 成長率 (%) 図 1-1 経済成長率の推移 出典 : International Monetary Fund 4

6 180, , ,000 総自動車登録台数 ( 千台 ) 120, ,000 80,000 60,000 40,000 20, 一人当たり実質 GDP( $) 図 1-2 一人当たり実質 GDP と自動車登録台数の推移 出所 : World Bank World Development Indicator, Transport Research Wing, Ministry of Road Transport & Highways, Government of India, New Delhi ROAD TRANSPORT YEAR BOOK ( ) 総自動車登録台数 ( 千台 ) 180, , , , ,000 80,000 60,000 40,000 20,000 0 Two Wheelers Cars, Jeeps and Taxis Buses Vehicles Others 図 1-3 自動車登録台数の推移 出所 : Transport Research Wing, Ministry of Road Transport & Highways, Government of India, New Delhi ROAD TRANSPORT YEAR BOOK ( ) 5

7 3,000,000 2,500,000 2,430,105 2,769,629 2,679,194 販売台数 ( 台 ) 2,000,000 1,500,000 1,000,000 1,052,198 1,552,010 1,414,845 1,269,305 1,970, , 図 1-4 乗用車の販売台数の推移 出所 : Society of Indian Automobile Manufacturers 中国インドネシアタイインド 171 台 / 千人 図 1-5 千人当たり乗用車保有台数の比較 出所 : EDMC エネルギー 経済統計要覧

8 1.2. 運輸需要自動車の登録台数が増加し続けていることから明らかなように インドの運輸需要は伸び続けている 図 1-6 は貨物需要 図 1-7 は旅客需要の推移である インドの貨物需要は 1999 年に道路貨物が 4,670 億トンキロ 鉄道貨物が 3,050 億トンキロであったが 好調な経済成長によって 2011 年には道路貨物が 3 倍 鉄道貨物が 2 倍に増加した 道路貨物の運輸需要の伸びが顕著であり 相対的に鉄道からトラックにシフトしつつある インドは 詳細は後述するが 約 6 万 5,000 キロの鉄道網が整備されている一方で 鉄道の貨物料金が高く コスト面でトラックに遅れをとっている このため インドの鉄道は石炭 肥料 セメント等の製品が主要な貨物となっており その他はトラック輸送が担っている 旅客需要も 1999 年から道路旅客 鉄道旅客とも増加し続けており 貨物需要と同様に道路旅客の伸びが顕著である 1999 年は道路が 1 兆 8,316 億人キロ 鉄道が 4,307 億人キロだが 2011 年に道路が 3 倍 鉄道が 2 倍にまで増加した Road Transport Railways 億 tkm 図 1-6 貨物需要の推移 出所 : Transport Research Wing, Ministry of Road Transport & Highways, Government of India, New Delhi ROAD TRANSPORT YEAR BOOK ( ) 7

9 Road Transport Railways 億人 km 図 1-7 旅客需要の推移 出所 : Transport Research Wing, Ministry of Road Transport & Highways, Government of India, New Delhi ROAD TRANSPORT YEAR BOOK ( ) 1.3. エネルギー消費量インドの一人当たり実質所得が増加し 自動車登録台数が伸び続け 運輸需要が拡大するのと同時にエネルギー消費量も増加し続けている 特に インドの運輸部門で最も使用されているディーゼルの増加が著しい 図 1-8 は インドの運輸部門のエネルギー源別エネルギー消費量である 1980 年以降 インドの主要燃料はディーゼルであり 近年もディーゼル燃料の消費量が非常に大きく伸びている 図 1-9 に示すよう 道路輸送のエネルギー源別エネルギー消費量をみれば 大量のディーゼル燃料が消費され 年々増加し続けていることがわかる こうした傾向は 石油天然ガス省傘下の PPAC (Petroleum Planning & Analysis Cell) が公表している燃料油の消費データからもうかがえる 図 1-10 は PPAC が公表している月次のガソリンと軽油の消費量の推移である インド国内では ガソリンや軽油に補助金が支給され 政策的に低い価格に誘導されていたが 近年補助金が撤廃された しかし 2000 年以降の傾向を見る限り 補助金撤廃による消費量の変化は見えない 8

10 石炭 天然ガス LPG ガソリン ジェット燃料 ディーゼル 電力 80,000 70,000 60,000 50,000 ktoe 40,000 30,000 20,000 10, 図 1-8 運輸部門のエネルギー源別エネルギー消費量の推移 出所 : IEA Energy Balances of Non OECD 2014 天然ガス LPG ガソリン軽油 出所 : IEA Energy Balances of Non OECD 2014 図 1-9 道路輸送のエネルギー消費量 9

11 軽油 ガソリン 7,000 6,000 5,000 4,000 千 t 3,000 2,000 1, /4 2001/ /4 2002/ /4 2003/ /4 2004/ /4 2005/ /4 2006/ /4 2007/ /4 2008/ /4 2009/ /4 2010/ /4 2011/ /4 2012/ /4 2013/ /4 2014/10 出所 :Petroleum Planning & Analysis Cell 図 1-10 ガソリンと軽油の消費量の推移 1.4. 運輸部門の燃料補助政策及び省エネ政策動向インド政府は 運輸部門における道路交通 ( 乗用車 バス トラック 二輪車等 ) の分野において以下のような政策を実施している 長年にわたり燃料に対する補助政策を継続してきた 主に 低所得者層への支援として 政策的にガソリンや軽油の価格を低い水準に抑えてきたのである しかし 補助金支給は省エネの観点には逆行するものであり エネルギー消費を増加させる要因となっていた 所得水準に関わらず ガソリンや軽油の価格が国際市況や周辺国と比較して低位に維持されてきたため 自動車の保有率が高い高所得者層が消費量を増やすドライバーとなった 近年では中間層も乗用車の保有率が高まり 上述のように乗用車の販売台数 登録台数ともに大きく増加 エネルギー消費量も伸び続けている こうした状況に対し インド政府は燃費基準の導入を 2005 年から検討しており 2016 年からこれを導入することを 2014 年 1 月に公示した 乗用車の増加は大気汚染の原因となり 特に近年の急激な増加により大都市圏を中心とした深刻な大気汚染を発生させている インドでは 1990 年代から段階的に Bharat Stage(BS) と呼ばれる排出基準を導入 大気汚染対策を進めている 10

12 燃料補助金インドでは 長年にわたり燃料価格に対する補助政策によって統制価格が維持されてきた これは 農業従事者が輸送用や灌漑用ポンプ等で消費する石油製品や乗用車の燃料等 全石油製品に適用され 低所得者層への補助制度として機能していた 1960 年代に輸入平衡価格 (IPP, Import Parity Price) 方式をコストプラス方式の管理価格 (APM, Administered Pricing Mechanism) 方式として 全石油製品に適用された価格設定に変更しが 1970 年代は両方式の間で揺れ動いた そして 1997 年に APM を段階的に廃止することが決定され 4 年後の 2002 年に全廃されることになった そして 2002 年に LPG と灯油を除き APM が廃止されたが 国営石油会社による寡占市場のため 政府が価格決定に関与し続けた 具体的には 石油天然ガス省傘下の PPAC(Petroleum Planning Analysis Cell) が市場価格の動向を踏まえて必要に応じて価格改定がなされてきた この価格決定の際に 州政府は関与していないが 州政府は物品税等の燃料価格に上乗せされる税制の決定権限をもっている しかし 図 1-11 に示すように 国際価格は 2004 年から上昇し続け 2008 に 120 ドル /bbl の水準にまで達したが 統制価格は原油コストや精製コスト 経費の合計を下回る水準であった このため 政府 上流企業 国営石油会社がそれらの損失を補填していたが 国営石油販売会社 (Oil Marketing Company, OMC) の回収不足は 持続不可能な水準に達した 図 1-12 は軽油価格と補助金額の推移 図 1-13 は損失補てんのための政府 上流企業 国営石油会社の負担額である 図 1-12 に示すように 2008 年に市場価格が急激に上昇したことで統制価格との差が拡大し これによって巨額の補助金が投じられたことがわかる また 2011 年以降も同様の状況にある さらに 図 1-13 に示すように インド政府及び上流企業は 市場価格が上昇することで巨額の負担が生じており 最も負担が大きい 2013 年には 1 兆 6000 億ルピーに達した こうした状況に対し インド政府は諮問委員会を組織 補助金政策の見直しが議論されてきた 2006 年に Rangarajan Committee が燃料価格を市場価格にすべきと提言し 2010 年の Parikh Committee 2011 年に Nilekani Task Force そして 2012 年には Kelkar Commttee が同様の提言をインド政府に行っている こうした提言の背景として 政府の補助金負担による財政赤字を積み重ねたことで財政を圧迫していたことが挙げられる 図 1-13 に示したように 政府は石油債券を発行し 損失の補てんを行っているが その額は小さなものではない IISD(2012) や Rahul (2013) が指摘しているように 燃料補助金は本来低所得者層のための政策であったにもかかわらず 燃料を大量に所得するのは高所得者層であるため 結果的に高所得者層をより手厚く補助するものになっていた 結果として 2010 年にガソリン価格は規制緩和し ディーゼルについては 2012 年から段階的に補助金を減らし 2014 年 10 月には原油価格の急落を受けて完全に軽油補助金と 11

13 価格統制制度を廃止した 他方 灯油 LPG 肥料といった低所得者層と農業従事者がより必要とする物資については 補助金が継続することとなり より低所得者層向けの支援策として現在は存続している 140 原油価格 (Indian Basket, $/bbl) /4 2000/ /6 2002/1 2002/8 2003/3 2003/ /5 2004/ /7 2006/2 2006/9 2007/4 2007/ /6 2009/1 2009/8 2010/3 2010/ /5 2011/ /7 2013/2 2013/9 2014/4 2014/11 出所 :Petroleum Planning & Analysis Cell 図 1-11 原油価格 (Indian Basket) の推移 図 1-12 軽油価格と補助金の推移 出所 : Rahul Anand, David Coady, Adil Mohommad, Vimal Thakoor, and James P. Walsh (2013) The Fiscal and Welfare Impacts of Reforming Fuel Subsidies in India, IMF Working Paper 12

14 Rs. in Crore (1000 万ルピー ) 180, , , , ,000 80,000 60,000 40,000 20, 図 1-13 under-recovery の推移 インド政府による負担 (2009 年から石油債権を発行 ) OMCs の負担 ( 損失 ) 上流企業 (Oil, ONGC & GAIL) の負担 Total Under Recovery 180, , , , ,000 80,000 60,000 40,000 20,000 0 Rs. in Crore (1000 万ルピー ) 出所 : Ministry of Petroleum & Natural Gas, Government of India, Basic Statistics on Indian Petroleum & Natural Gas 燃費基準図 1-4 に示したように インド国内では年間 267 万台の乗用車が販売されており 大量のエネルギーを消費している しかし インド国内には燃費基準が導入されておらず 石油の大部分を輸入に頼るインドにとって 乗用車の燃費を向上させることは喫緊の課題である 電力省傘下の BEE(Bureau of Energy Efficiency) は 乗用車の燃費を改善するために 2005 年から 省エネ法に基づく燃費規制の導入を検討してきた 当初より BEE は自動車メーカーに対して 企業別平均燃費 (CAFC, Corporate Average Fuel Consumption ) を 2015 年から導入し 2020 年から CAFC を引き上げることを検討していた また 乗用車に対して 5 段階評価を含むラベリング制度の導入を検討 消費者が自動車を購入する際に参照できるように添付することを検討していた また 自動車燃費規制には 第一に車体重量とサイズを大きくすることへの逆インセンティブが必要であること 第二に不遵守の場合の罰則が必要であること そして第三に不遵守罰則が十分な抑止力となることが必要であるとした 加えて 燃費規制によって省エネを促進するためには 規制を野心的に設定しな 13

15 いと むしろ BAU よりも低水準で新車燃費を推移させることになりかねないため 慎重な目標設定も必要であるとしていた しかし 2011 年に BEE からコンサルテーションペーパーが公表され 2014 年 1 月に燃費基準が公示されるまで BEE が導入を検討してから 9 年の時間を要した これは 特に民族系メーカーが BEE が検討していた CAFC を達成することが難しいため 燃費基準の導入に反対したためである 2014 年 1 月に公示された基準値は 2016 年の CAFC が 18.2km/ リットル CO2 換算した場合に 129gm/km と設定された また 第 2 段階として 2021 年に CAFC を 21km/ リットル CO2 換算した場合に 113gm/km とした 1 この基準値については 販売される乗用車の主力が小型車のインド市場において 将来の経済成長によって消費者が大型車へ乗り換えが進んだ場合 小型車の販売比率が小さいメーカーには厳しい目標値になるとの見方がある 図 1-14 は BEE のワークショップ資料で示された燃費基準と各メーカーの対応状況である 図中に 2009 年 -10 年の燃費水準が示され 併せて第一段階 第二段階の燃費規制の水準が示されている これらの水準上に各メーカーの CAFC 値がプロットされている 同図から マルチスズキやホンダ等の小型車の比率が高いメーカーは既に 2017 年 -18 年の水準を達成していることがわかる 一方で トヨタやメルセデスベンツ マヒンドラ等のメーカーは 2012 年 -13 年の時点では燃費規制の水準に達していないことがわかる 出典 : ワークショップ発表資料 図 1-14 インドの燃費基準と各メーカーの燃費性能 1 REGD. NO. D. L /99 14

16 燃費基準と併せて BEE は燃費ラベルの添付を検討している 2009 年から SIAM が自主燃費ラベルを導入しているが これを置き換えるものになる ラベルには 自動車の燃費を 5 段階で評価し明示される 図 1-15 は 2011 年の BEE のコンサルテーションペーパーで示されたラベル案である 出典 :BEE(2011) CONSULTATION PAPER 図 1-15 インドの燃費ラベル案 排出基準インドでは 長年自動車の排気ガスによる大気汚染が大きな問題となってきた これは主に三つの方法で軽減することが可能である 第一に 燃焼する前の時点で燃料から汚染の原因物質 ( 硫黄分など ) を取り除くことで 排気ガスからの汚染物質を減少させることができる 第二に 自動車運転時に不要な燃料消費を減らすことで 排気ガスそのものを減少させることができる 第三に 排気ガスを社外に放出する前の時点でフィルター等を用いて大気中に汚染物質を除去することで大気汚染を防ぐ方法がある インドでは 排気ガス規制の導入や 都市部における圧縮天然ガス車 (CNG) を導入することで 排気ガス対策に取り組んできた 現在インドでは Bharat Stage(BS) と呼ばれる排気ガス規制が導入されており現在 インド全土で BS-III(EU の EURO3 に相当 ) が導入されており 主要都市では BS-IV(EURO4 相当 ) となっている 今後 BS-IV を全国展開するほか 主要都市から BS-V(EURO5) 相当が導入される 2014 年 5 月に発表された Auto Fuel Policy では 2017 年までに BS-Ⅳを全国に展開 主要都市での BS-Ⅴの導入を 2019 年からとしている これに伴って 燃料の品質を改善していくた 15

17 めに 製油所に対して総計 8,000 億ルピーの投資が必要である指摘している このための資金について 一部が燃料価格に含まれているが 製油所へのヒアリングしたところ 設備改修費用は自己負担を予定し 燃料価格には転嫁しない予定とのコメントがあった これは ガソリンや軽油への燃料補助金が撤廃されたことで 石油精製企業間の競争が促進されているといえる こうした取り組みの結果として ガソリンの硫黄分は 2000 年から 2010 年にかけて 2000ppm から 150ppm に減少し 軽油の場合 10,000ppm から 350ppm まで下げることができた 将来的に 段階的な排ガス規制が進むことで 大気汚染の改善が見込まれる 1.5. インド運輸部門の課題文献調査やヒアリング調査を踏まえ インドの運輸部門の省エネルギーを促進するための課題について整理する 1. 不透明な燃料価格の決定過程 原油価格の下落によって燃料補助制度が撤廃されたが 今後原油価格が上昇した場合に復活する可能性が残る この理由として 燃料価格への補助制度が低所得者層への支援という側面があり 常に政治問題となるためである 燃料価格に上乗せされる物品税は 州ごとに差がある このため 安い州の州境沿いに給油待ちの行列ができ 渋滞や燃費低下の原因となっている 連邦政府が現在 物品税の統一化に向けて州政府と交渉中である こうした燃料価格政策の不透明さは 自動車を購入する際の燃料選択に影響を与えている インドの多くの消費者は 自動車のランニングコストに敏感であり ガソリン 軽油 CNG LPG の価格の見通しが重要な要素となる 同時に 自動車メーカーにおいても 燃費が良く 環境性能の優れた自動車を開発するためのインセンティブが阻害されている 自動車メーカーのリソースは限られており 今後の消費者の燃料への選好を踏まえた 中長期的な観点から燃費が良く 環境性能の優れた自動車を開発するための投資を困難にしている さらに 運輸部門の省エネルギー 環境保全対策を阻害している 燃料価格が低く抑えられることで 需要側において燃費が良く 環境性能の優れた自動車 バス トラックへの買い替えが進まず 補助制度がそうしたインセンティブを抑制する省エネバリアとなっている 2. 原油価格下落による省エネ意識の後退 原油価格が下落したことで燃料補助制度の撤廃が決定されたが これによる燃料消費量の変化は大きくなかった インドでは 今後も経済成長が継続した場合 乗用車の保有率が上昇し 燃料消 16

18 費量が増加し続けると見込んでいる インドで導入が予定されている燃費規制の影響について 燃料供給事業者は今後も燃料需要が減少するとは想定していない こうした中で 原油価格の下落によるインド国内の燃料価格の下落は 省エネ意識を後退させる要因となる 3. 燃費規制と排ガス規制による自動車価格の上昇とインセンティブの欠如 BEE は 2017 年から燃費規制の第一段階を導入 2022 年から第 2 段階へ移行する 図 1-14 に示したように 第 2 段階の燃費規制は非常に厳しい水準であり 自動車メーカーが対応するためには技術開発が必要となる また インドは都市部を中心に大気汚染が深刻であり 1990 年代後半から段階的に排ガス規制が強化されてきた 燃料については 段階的に燃料品質の改善が進められている 今後は 規制強化に合わせて自動車に排ガス浄化装置の装備等 コストがかかる対策が必要となる また 一部のガスパイプラインが整備された州や大都市圏では CNG 車の普及促進策が導入されている こうした規制によって燃費水準の改善や大気汚染の改善が見込まれるが 規制に対応した自動車の価格を上昇させる 一方で インドの消費者は価格に敏感であり 燃費性能に優れた乗用車の普及を妨げる要因となってします また こうした乗用車の普及を促すためのインセンティブ制度がないため より安く燃費性能に劣る乗用車や中古車の購入が選択される 4. 道路インフラの容量不足と燃料品質の確保 インド国内では 年間 200 万台以上の乗用車が販売され これを超える台数の二輪車が販売されている このため 特に大都市圏を中心に昼間時間帯の渋滞が常態化いている このため インド政府は高速道路の整備などを進めているが 需要に追い付いていない こうした渋滞の頻発は 乗用車の燃費を悪化させる大きな要因の一つであり 交通流対策やモーダルシフトが必要である また インド国内に供給されている燃料の品質には課題がある 第一に BS-IV の燃料が都市部で販売されていても BS-IV が導入されていない地域で給油し 都市部に移動すると BS-IV 販売地域でも想定した大気汚染防止効果が得られないことが挙げられる この点からも全国で BS-IV を展開することが急がれている 第二に 製油所で BS-IV や BS-V を遵守した高品質な燃料が精製されても 燃料タンクやパイプライン ガソリンスタンドといったインフラ全体で油質を管理する制度や能力が無いため 消費されるまでに燃料が劣化するという問題がある これに対し インド政府としては Auto Fuel Policy の中で 油質に管理に注力していくとしている 17

19 5. 省エネ意識の啓発と教育 インドのドライバーは 自動車のランニングコストに敏感ではあるが 省エネには繋がっていない また ライセンスを取得する際に 安全かつ 効率的な運転とメンテナンスのための教育が不十分な状態である BEE は 燃費基準の導入とともに 燃費ラベルの導入を計画している これによって 消費者が自動車を購入する際に低燃費車を選択することを期待している 18

20 2. グジャラート州における燃料消費実態と省エネ行動に関するアンケート調査 2.1. 概要委託事業の一環として グジャラート州の二輪車 乗用車保有者の燃料消費実態及び省エネ行動に関するアンケート調査を実施した アンケート質問は Appendix 1 結果の詳細については Appendix 2 を参照されたい ここでは アンケート結果のうち インドの運輸部門の省エネ政策及び燃費性能に優れる乗用車の普及に関連する結果の概要を示す 目的インドの運輸部門では 今後の経済成長によって乗用車への需要が急激に増加すると予測されており 多くの自動車メーカーがインド市場に参入している 一方で インドは石油資源の多くを輸入に頼っており エネルギー安全保障を強化するためにも 国内の運輸部門に対する省エネ政策として乗用車の燃費規制の導入が重要となるが どの程度の燃料が消費されているのか どの程度の距離を走行するのか 保有状況や燃費 燃料価格への反応等といった燃料消費実態に関する知見は不足している さらに インドの消費者は燃料価格に敏感と言われているが 燃料価格の変動によってどの程度燃料消費量が変化するのかは定量的なデータが不足している そこで 本事業では インドグジャラート州において 二輪及び四輪保有者を対象としてアンケート調査を実施した その理由として グジャラート州はインドのモディ首相が州知事を務めていた時代に他の地域と比較して急速な発展を遂げた地域の 1 つであり 今後のインドの省エネ政策を検討する上で 典型的な地域の 1 つと捉えることができることが挙げられる 当然 インドの各地域に対してアンケート調査を実施することも検討したが 地域を増やすことに依る小サンプルの弊害を回避するために 特定の地域に絞る方針をとった 方法アンケート調査は グジャラート州の Ahamedabad, Anand, Bhavnagar, Rajkot, Baroda, Surat, Mehsana, Bhuj の 8 地域で実施 無作為に抽出された二輪車または乗用車を保有する 18 歳以上の成人を対象とし 調査員による聞き取り調査をおこなった アンケート表は Appendix 1 に示したように アンケート対象者に対して 属性 二輪車及び乗用車の保有 利用状況 燃料消費量 燃料費等の設問への回答を依頼した その結果 アンケートの回収数は 1109 であった 2.2. 分析結果 アンケート対象者の属性アンケート対象者の属性について 世帯人数 年齢階層 所得について以下に示す 19

21 図 2-1 は世帯人数である 4 人家族が最も多く 35% を占め ついで 5 人家族 6 人家族が多い 図 2-2 に回答者の年齢階層である 21~30 歳の回答者が最も多く ついで 31 歳 ~40 歳が多い また 全体として女性は少数である 図 2-3 に示す通り 所得別では 月間所得が 3 万 ~5 万ルピーの層が最も多く ついで 3 万ルピー以下の層が多い その他のアンケート結果も踏まえると アンケートの回答者は 都市部及び近郊に住む乗用車を保有できる裕福な層であり 夫婦と一人から二人の子供がいる若い世代が典型的な回答者となっている 度数 人 2 人 3 人 4 人 5 人 6 人 7 人 8 人 9 人 10 人 11 人 図 2-1 世帯人数 男性 女性 400 度数 ~20 歳 21~30 歳 31~40 歳 41~50 歳 51~60 歳 61 歳以上 図 2-2 年齢と性別 20

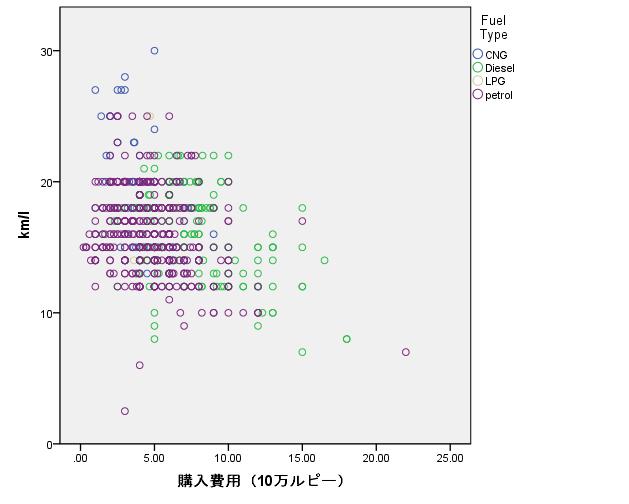

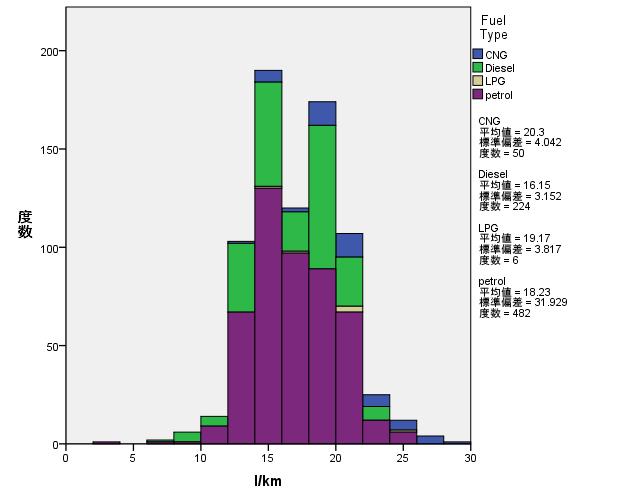

22 万ルピー以下 3 万 ~5 万ルピー 5 万 ~10 万ルピー 10 万 ~20 万ルピー 度数 20 万 ~50 万ルピー 図 2-3 所得階層 二輪及び乗用車の保有 利用状況二輪車及び乗用車の保有状況 及び利用状況についての設問への回答の概要を示す 表 2-1 は二輪車及び乗用車の保有状況をクロス集計したものである 回答結果から乗用車一台 二輪車一台 ~ 二台を所有している回答者が多数である このため 乗用車の保有者は 引き続き二輪車を保有していることがわかる 次に 回答者が所有する乗用車のメーカーについての回答結果を図 2-4 に示す インドの自動車メーカーシェアはマルチスズキが最も大きく 次いで韓国の現代自動車 インドのタタ自動車の順となる 今回のアンケート調査でも同じ傾向となっており マルチスズキが 46.79% と最も大きなシェアとなっている 次いで 現代自動車 タタ自動車のシェアが大きい結果となった また 保有している乗用車の燃料種別や購入価格 燃費についての設問への回答を図 2-5 に示す 横軸は購入費用 縦軸が燃費 点は燃料種別ごとに色分けしている 図 2-5 から ディーゼル車の購入費用がガソリン車よりも高い傾向にあることがわかる 一方で 燃費をみると ディーゼル車はガソリン車と同等 あるいは燃費が悪いことがわかる したがって 一般的にディーゼル車の方が燃費性能に優れ 先進国では大気汚染対策を施したクリーンディーゼルが普及しているが インドではガソリン車よりも燃費で劣るディーゼル車が高い価格で販売されているといえる このことは 図 2-6 に燃料別の燃費を示すように 今回の調査対象者の保有するガソリン車の燃費の平均値は 18.23km/l であるが ディーゼルは 16.15km/l であることからも指摘できる ただし 図 2-6 にあるように ガソリン車の燃費の分散は大きく 最頻値は 15km/l 21

23 台である 一方で ディーゼルの分散は小さく 最頻値は 20km/l 弱となっている このことから ディーゼル車については 旧型の燃費の悪い乗用車が使用されている可能性や車種ごとの差異が存在する可能性が示唆される こうした点について 図 2-7 にメーカー別 燃料別の燃費の分布を示す 表 2-1 二輪車と四輪車の保有状況 No. of four wheelers in the household 合計 No. of two wheelers in the household 合計 図 2-4 メーカー別保有状況 22

24 図 2-5 燃料別購入費用と燃費の散布図 図 2-6 燃料別燃費の分布 23

25 図 2-7 メーカー別 燃料別の燃費の分布 24

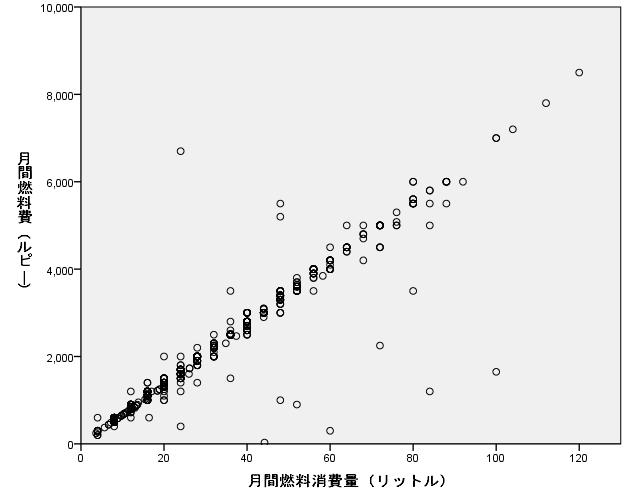

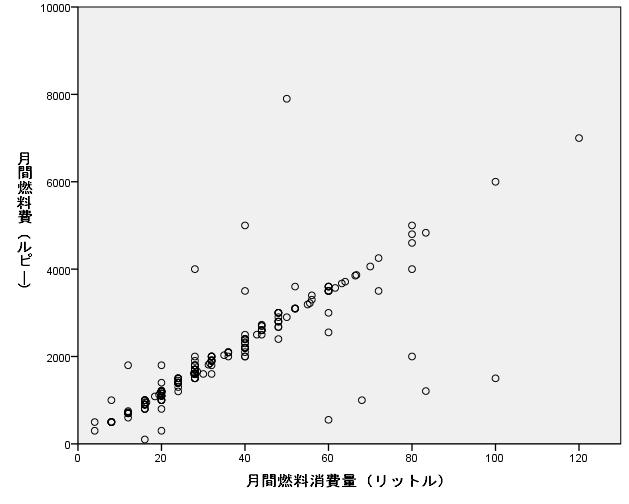

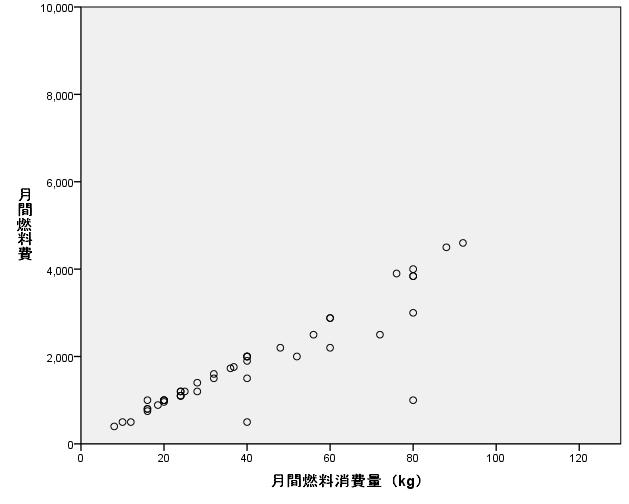

26 続いて 二輪車と乗用車の利用状況について示す 表 2-2 は それぞれの一週間の走行距離をクロス集計したものである 二輪車で最も多いのが週に 100km 程度という回答が多く 次いで 150km 200km となっている 乗用車では 100km が最も多く 次いで 250km が多い 今回のアンケート対象者の大部分が都市及び都市近郊に居住しているが その多くが週に 100km から 200km 程度の距離を二輪車または乗用車で移動していることがわかる こうした移動に必要となる燃料消費量と燃料費の月間平均を表 2-3 に示す アンケートの結果を見ると ガソリンの燃料消費量よりも軽油の消費量が多いことがわかる 一方で 燃料費をみると ガソリンの方が軽油よりも大きい この理由として グジャラートでは軽油価格がガソリン価格より低く 2014 年 10 月まで燃料補助金によって政策的に軽油価格が低位に据え置かれていたことが挙げられる また 燃料補助金撤廃後も 各種の税制等の要因によって軽油の方がガソリンよりも安価である さらに CNG をみると ガソリンや軽油よりもさらに燃料費が安い こうした点について 図 2-8 にガソリン消費量と燃料費 図 2-9 に軽油消費量と燃料費 図 2-10 に CNG 消費量と燃料費を示すように これらの傾きを見れば明らかである 表 2-2 一週間当たりの二輪車と四輪車の走行距離のクロス集計表 乗用車 Up to more 合計 二輪車 Up to more 合計 表 2-3 燃料別月間平均消費量と月間平均燃料費 月間平均燃料消費量月間平均燃料費 ガソリン 30.8 リットル ルピー 軽油 34.2 リットル ルピー LPG 34.9kg ルピー CNG 42.9kg ルピー 25

27 図 2-8 ガソリン消費量と燃料費の散布図 図 2-9 軽油消費量と燃料費の散布図 図 2-10 CNG 消費量と燃料費の散布図 26

28 あわせて 乗用車のメンテナンスについて質問した その結果 全体の 65% が 3 カ月に一度 30% が 6 カ月に一度 自動車をなんらかのメンテナンスあるいは修理に出している また 67% がメンテナンスや修理の際にメーカー公認のサービスセンターを利用し 30% がそれ以外の修理工場を利用していることがわかった また 年間のメンテナンス及び修理費用が 3000~5000 ルピーという回答が 46% で最も多く ついで 5000~1 万ルピーという回答が 45% を占めている 図 2-11 メンテナンス頻度 図 2-12 メンテナンス依頼先 図 2-13 年間メンテナンスコスト 27

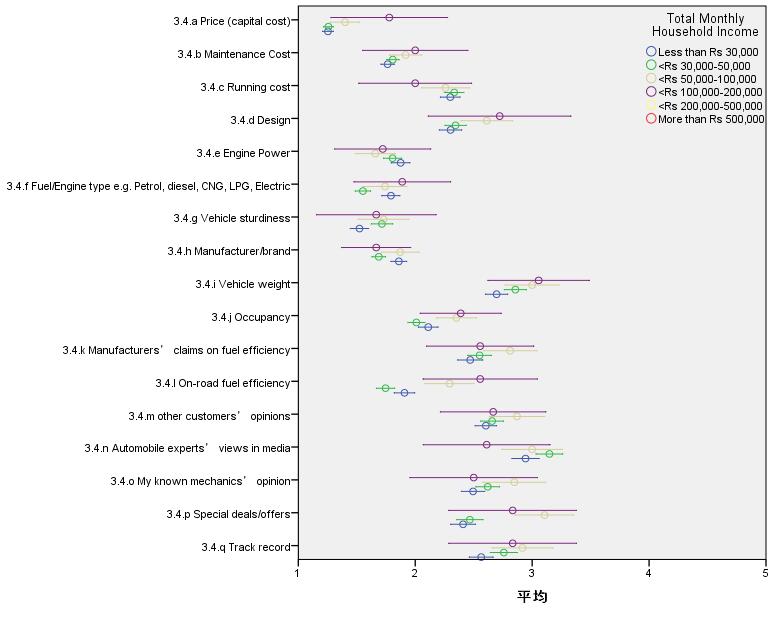

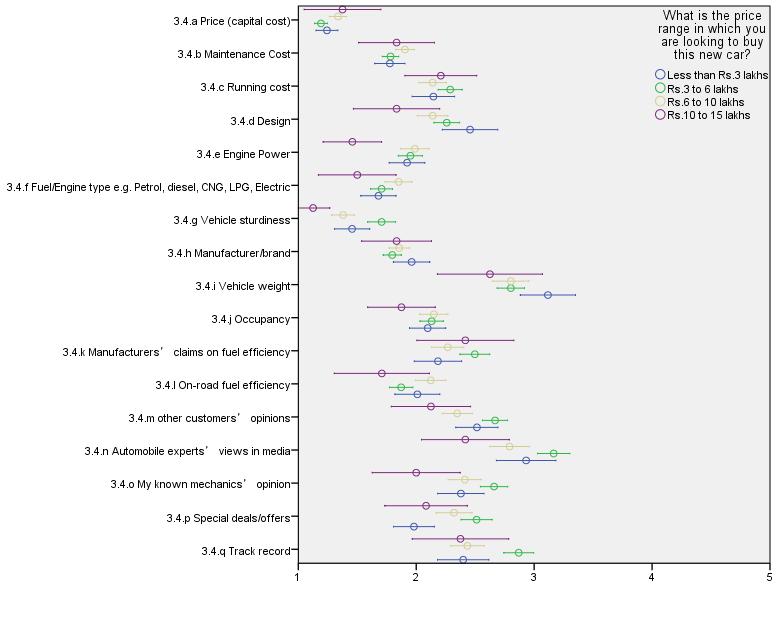

29 乗用車の購入段階における燃費選好続いて 乗用車の購入段階における検討事項について質問した 図 2-14 は乗用車の購入理由を尋ねた結果である アンケート回答者 1109 名のうち 627 名が乗用車の購入または買い換えを検討しており その理由として 家族のニーズを満たすため という回答が最も多く 次いで 通勤 や 様々な社会的ニーズを満たすため といった回答が多かった こうした買い換えの際の予算と所得水準をクロス集計した結果が表 2-4 である 月収が 3 万ルピー以下では 30 万から 60 万ルピーが最頻値となっている また 月収が 3 万ルピーから 5 万ルピーの層も同様の水準が最頻値である 次に 自動車を購入する際 どの燃料を選択するか質問したところ 図 2-15 に示すように ガソリン車 ディーゼル車 そして CNG 車でほぼ三等分となった また 所得別に見ると図 2-16 のようにディーゼル車の購入を検討している回答者の所得が高い傾向にある さらに 図 2-17 に示すように 購入予算を多めに設定していた また 図 2-18 に示す通り ディーゼル車が現在の自動車利用状況において最も長距離を走行する傾向がある 他方 ガソリン車と CNG 車の間には 所得や購入予算の傾向に違いは見られなかった そして 乗用車の購入段階において重視する点として 価格や維持費用 メーカーや燃費など 17 の点について 5 段階で評価するように質問した その結果を 図 2-20 は所得水準別に整理し 図 2-21 は購入予算別に整理した (1 が最重視 5 が重視しない ) 当然 最も重視するのが初期費用としての自動車の価格であり メンテナンスやランニングコストのように価格やコストが重要な要素であることが確認された また こうした点は所得水準や購入予算で大きな差は無いと言える 性能面ではエンジンパワー 燃料のタイプ 頑丈さ そして実質燃費を重視している 加えて メーカーも購入時の重要な検討事項となっている しかし 所得水準や購入予算によってこうした点を重視するか否かには若干の差異が存在する 図 2-20 から 所得が少ない層は車体価格や燃費をより重要視していることがわかる さらに 図 2-21 に示す通り 自動車の購入予算を多めに設定している層の方が 燃費を重要視していることがわかる したがって 乗用車の購入段階において 消費者は価格を重視し 購入後のランニングコストに影響する燃料選択も含めて乗用車の購入を検討している 同時に 燃費も重視する点の 1 つであり 主に経済的要因によって燃費を重視している 燃費性能が優れた乗用車を選好する素地はあるが 予算上の制約によって その他の要因を優先していると考えられる また 新たに乗用車を購入する際にこれまでと同じサイズの乗用車を購入するかという問いに対して 大部分が異なるサイズを検討していると回答している このことは 将来的に小型乗用車から大型乗用車へと消費者の選好が移行していくことを示唆しており 今後の経済成長による所得の上昇は 燃費性能で劣る大型乗用車の普及によって全体的な燃費の悪化が予見される したがって 小型乗用車だけでなく 燃費性能に優れた大型乗用 28

30 車の普及を促すことが将来的な課題といえる 図 2-14 自動車の購入理由 表 2-4 所得と購入予算のクロス集計表 3.5 What is the price range in which you are looking to buy this new car? Less than More than Rs.3 Rs.3 to 6 Rs.6 to 10 Rs.10 to Rs.15 lakhs lakhs lakhs 15 lakhs lakhs 合計 0.7 Total Monthly Household Income Less than Rs 30,000 <Rs 30,000-50,000 <Rs 50, ,000 <Rs 100, , 合計

31 3 万ルピー以下 月間所得 3 万 ~5 万ルピー 5 万 ~10 万ルピー 万 ~20 万ルピー % 20% 40% 60% 80% 100% 購入予算 30 万ルピー以下 30 万 ~60 万ルピー 60 万 ~10 万ルピー 10 万 ~15 万ルピー 15 万ルピー以上 図 2-15 月間所得別自動車購入予算 30% 32% ガソリン車 ディーゼル車 CNG 車 38% 図 2-16 購入希望車種 ( 燃料別 ) ガソリン車 ディーゼル車 CNG 車 % 20% 40% 60% 80% 100% 3 万ルピー以下 3 万 ~5 万ルピー 5 万 ~10 万ルピー 10 万 ~20 万ルピー 図 2-17 購入予定車種と月間所得 30

32 ガソリン車 ディーゼル車 CNG 車 % 20% 40% 60% 80% 100% 30 万ルピー以下 30 万 ~60 万ルピー 60 万 ~10 万ルピー 10 万 ~15 万ルピー 15 万ルピー以上 図 2-18 購入予定車種と購入予算 ガソリン車 ディーゼル車 CNG 車 % 20% 40% 60% 80% 100% 50km 以下 100km 程度 250km 程度 500km 程度 750km 程度 1000km 以上 図 2-19 購入希望車種と現在の自動車走行距離 ( 週 ) 31

33 図 2-20 所得階層別自動車購入時に検討するポイント 32

34 図 2-21 購入予算別自動車購入時に検討するポイント 33

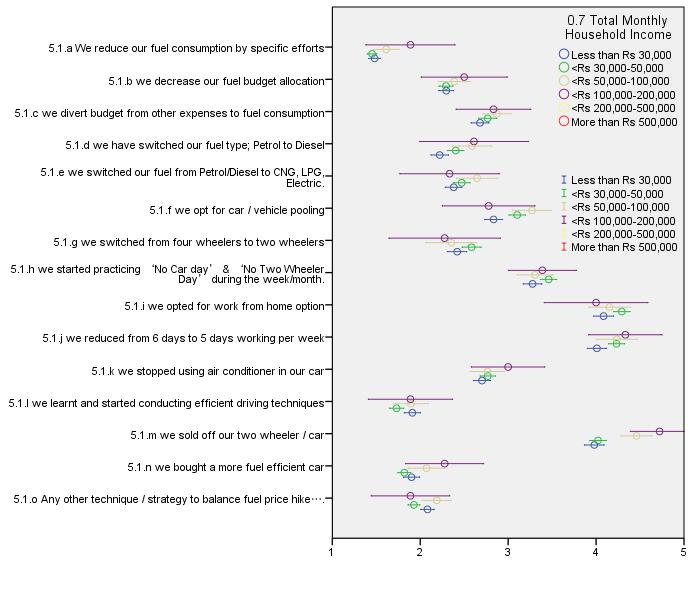

35 燃料価格の変動による行動変化既に述べたように インドの燃料価格は国際市況価格の急落によって下落し 燃料価格高騰対策としての燃料補助金も撤廃された 一方で インドの消費者は燃料価格に敏感であり これが再度上昇したときにどのような行動変化があるのかを調査することは意味がある アンケートにおいて 燃料価格が上昇した場合にとる行動について 16 の選択肢を示し これらについて 5 段階での評価を尋ねた この結果を 図 2-22 に示す (1 が行動する可能性が最も高い 5 が行動しない ) 結果を見ると 燃料価格上昇した場合 燃料消費削減に何らかの対策をとる意識がり 所得が少ない方がより積極的に対策をとる傾向にあることがわかる 具体的な対策としては 燃費のいい運転方法に最も関心があることがわかった これは どの所得階層でも同様である 次いで 低燃費自動車への関心が高く 同時に乗用車の燃料を変更するために乗用車の買替えを検討すると示唆される ただし 乗用車の利用そのものを減らすたようなライフスタイルの変化には消極的である 自動車を手放すことは検討すらされないが 四輪車から二輪車にシフトするということにも消極的である さらに 近所同士での相乗りをするということにも消極的であるように 乗用車の利便性を損なうことは極力避けようとする意識が強いといえる したがって アンケートの結果から 省エネを促進するためには 乗用車の燃費性能を改善し 市場に普及させることの重要性が示唆される これは 多くの消費者が利便性を損なうことを避けようとしているからである また 燃費を向上させる運転方法への関心があることから インド版エコドライブを普及させるための啓発や教育が重要である 34

36 図 2-22 所得階層別燃料価格高騰対策 35

37 公共交通の利用最後に 現在の公共交通の利用頻度について質問した 結果を図 2-23 に示す 最も多くの回答者が 週に一度利用する と回答している 次いで 週に二度利用する という回答と 全く利用しない という回答がいずれも 16% ほどになっており 一週間に三回以上利用すると答えた回答者は 2% に満たない 最も利用されているのは オートリキシャー (58%) で 次いでバス (31%) となっている また 燃料価格が上昇した際に公共交通の利用を増やすかという質問の結果を図 2-24 に示す これに対して 63% が否定的な回答を示した このことは 二輪車または乗用車を所有している人にとっては 燃料価格が上昇しても 公共交通に乗り換えることで支出を抑えようとする意識は低いことがうかがえる したがって 今回の限定的な調査から 二輪車及び乗用車を所有している場合 燃料価格が上昇した場合であってもモーダルシフトの可能性が低いことが示唆される ただし グジャラート州では メトロを初めとする公共交通機関の整備が途上であり こうしたインフラが形成されることで モーダルシフトを検討する余地が生じる可能性はある 図 2-23 公共交通機関の利用頻度 図 2-24 公共交通機関へのシフト 36

38 2.3. 政策への示唆 アンケート調査の結果から次のような政策への示唆が得られた 1. 高価だが燃費の劣るディーゼル車の排除 インドではガソリン車よりも燃費で劣るディーゼル車が高い価格で販売されている ディーゼル車については 旧型の燃費の悪い乗用車が使用されている可能性や車種ごとの差異が存在する可能性が示唆される 燃料補助金撤廃後も 各種の税制等の要因によって軽油の方がガソリンよりも安価なため 燃費性能の低いディーゼルが残る余地が存在する 2. 燃費性能に優れた乗用車へのインセンティブ 自動車購入の際の初期費用も大きなファクターであり 低燃費自動車であっても初期費用の高い車種は敬遠されてしまう また 購入後のランニングコストに影響する燃料選択も含めて乗用車の購入を検討している このため 低価格で燃費性能に優れた乗用車の開発の促進や初期投資への経済的インセンティブを付与することで低燃費車の普及促進に大きく貢献する 3. 省エネ行動の啓発と普及 燃料価格が上昇しても 利便性を損なうような燃料支出を減らす行動を起こす意識は低い また 回答者の自動車利用が都市部での短距離移動がメインであるにも関わらず 公共交通の利用による燃料支出削減にも消極的である 一方で 低燃費の走行方法への関心は高く エコドライブの情報や講習会等で啓発と方法の普及が重要である 4. メンテナンスの際の啓発 インドの消費者の多くが定期的に自動車を修理やメンテナンスを行っている こうした機会をとらえ 消費者に対して燃費改善のための働きかけをする機会となる 37

39 3. モデル分析本章では燃料価格と消費者の乗用車選好の関係ならびにそれらの将来におけるエネルギー需要に与える影響を理解するために 分析モデルに基づいて得た試算結果について述べることとする 試算の前提として 燃料価格の変化と購入乗用車に関する消費者選好の変化に関して行ったアンケート調査を活用しモデル分析に反映させている なお アンケート調査の枠組み ならびにその結果については第 2 章で説明している 3.1. シナリオ分析の枠組み本分析ではアンケート結果に基づく燃料価格の変化に伴う消費者の乗用車選好への影響を TERI(The Energy and Resources Institute) の National Transport Demand and Energy Model に反映し 将来の乗用車エネルギー需要見通しを作成している TERI モデルはボトムアップ方式でエネルギー需要を分析するもので 旅客部門と貨物部門のエネルギー需要が分析可能である そのうち本分析で活用したのは乗用車モデルであり ストック燃費を新車販売と耐用年数から計算 走行距離を乗じエネルギー需要を求めるものである アンケート調査項目から 燃料価格の変化に関する9つの項目をシナリオ作成の前提として活用し それぞれの乗用車に関するエネルギー需要見通しを行う シナリオ分析にあたって 燃料別に異なる相対価格を以下の 9 つに関して想定した シナリオ 1.1: ガソリン価格がディーゼル価格よりも 25% 高価になった場合 シナリオ 1.2: ガソリン価格がディーゼル価格よりも 35% 高価になった場合 シナリオ 1.3: ガソリン価格がディーゼル価格よりも 50% 高価になった場合 シナリオ 2.1: ディーゼル価格がガソリン価格と同水準になった場合 シナリオ 2.2: ディーゼル価格がガソリン価格よりも 25% 高価になった場合 シナリオ 2.3: ディーゼル価格がガソリン価格よりも 50% 高価になった場合 シナリオ 3.1:CNG 価格がディーゼル価格と同水準になった場合 シナリオ 3.2:CNG 価格がガソリン価格と同水準になった場合 シナリオ 3.3:CNG 価格がガソリン価格よりも 25% 高価になった場合 アンケート調査では ガソリン乗用車 ディーゼル乗用車 CNG 乗用車に関する新車購入計画のある回答者に対して 各車種の燃料価格が変化した場合 購入車種を変更するか否かについて尋ねている 具体的にはガソリン乗用車を購入する計画がある回答者に対して ガソリン価格がディーゼル価格よりも 25% 上昇した場合 購入するのをディーゼル車 CNG 車 LPG 車 または電気自動車に変更する可能性とその場合の選好車種を尋ねるものである ガソリン乗用車の購入を変更しないと回答したものに対しては 追加的にガソリン価格がディーゼル価格と比較して 35% 上昇した場合の車種変更の可能性とその場合の選好を質問している 同様の質問をディーゼル乗用車 CNG 乗用車の購入計画のある回答者 38

40 に尋ねるものである アンケート結果は 年以降の車種構成の変化に反映させ エネルギー需要見通しを作成している この点は今後の検討課題とする グジャラート州で実施されたアンケート結果を前提とし インド全国の消費者が価格変化に同じ選好をもつと仮定した上で シナリオ分析を行っている点に留意されたい シナリオの前提となる 燃料価格別の水準は以下の通りである ガソリン :67.75 ルピー /liter ディーゼル : ルピー /liter CNG:44.90 ルピー /kg これらをキロカロリーベースに変換しガソリン価格を 1 としたディーゼルの価格は 0.76 CNG 価格は 0.4 となる ガソリンディーゼル CNG 図 3-1 燃料価格の相対水準比較 ( ガソリンを 1 とする ) インドにおけるガソリン乗用車 ディーゼル乗用車 CNG 車の燃費水準 ( ストックレベル ) 以下の通りである ガソリン乗用車 :18.23 km/liter ディーゼル乗用車 : km /liter CNG 乗用車 :20.3 km/kg これらをキロカロリーベースに変換しガソリン価格を 1 としたディーゼル車の燃費は 0.77 CNG 車は 0.98 となる 2 ガソリン ディーゼルのリッターから kcal への換算係数はそれぞれ 7,908(kcal/ リッター ) 9,095(kcal/ リッター ) であり 天然ガスの kg から kcal への換算係数は 9,000 (kcal/kg) とし相対価格水準を計算した 39

41 ガソリン車ディーゼル車 CNG 車 図 3-2 ストック燃費の比較 ( ガソリン乗用車を 1 とする ) 3.2. シナリオ分析の主要結果 BAU ケースインドの所得水準の向上と歩調を合わせ 将来的にも乗用車保有台数は継続して増加 現在の 1600 万台から 年には 8000 万台への自動車保有台数は増加する ( 図 3-3) 本分析において GDP は 年から 年まで 12 次 5 ヶ年計画で目標とする年率 9.2% で増加した後 年まで年率 8% で増加する想定とする BAU ケースにおける乗用車の燃料別車種構成は 年において ガソリン乗用車の占める割合が 66% と 年の 60% から拡大する一方 ディーゼル乗用車の割合は 年で 28% と 年の 36% から縮小する これはガソリンとディーゼルの相対的燃料価格差の解消 ならびにイニシャルコストの違いからガソリン車へのシフトが起きるとする見通しを反映するものである 乗用車 ( 百万台 ) 人キロ (10 億 ) 人キロ 80 乗用車ストック % 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% 2% 3% 3% 2% 2% 2% 3% 3% 3% 4% 36% 35% 32% 30% 28% 60% 60% 62% 64% 66% 電気 LPG CNG ディーゼルガソリン 図 3-3 BAU ケース : 自動車保有台数見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合( 右図 ) 40

42 2,000 PJ 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 2% 2% 1% 2% 42% 41% 38% 36% 34% 55% 56% 57% 60% 62% 電気 LPG CNG ディーゼルガソリン 図 3-4 BAU ケース : 乗用車のエネルギー需要見通し ( 左図 ) 燃料別乗用車エネルギー需要 割合見通し ( 右図 ) BAU ケースにおいて 乗用車のエネルギー需要は 年の水準から年率 8.8% で増加 年にはほぼ 5 倍の 1,890 PJ に達する 燃料別ではガソリン需要が同期間に 6 倍の 1,171 PJ ディーゼル需要は 4 倍の 646 PJ に達する見通しである BAU ケースにおいて電気自動車や CNG 車のエネルギー需要は 年において全体の 3.9% を占める程度である 以下 シナリオごとの主要結果を提示する 詳細な分析結果は Appendix 3 を参照されたい シナリオの主要結果 シナリオ 1.1: ガソリン価格がディーゼル価格よりも 25% 高価になった場合シナリオ 1.1 では 2031 年における燃料別のエネルギー需要はガソリンの割合が 49% と 年の 55% から縮小する見通しである ディーゼル価格のガソリン価格に対する相対水準が小さくなることから 年 BAU と比較してディーゼルに対する選好も微増するため エネルギー需要に占める割合も同年 39% と微増する なお 本シナリオにおいて BAU 比で最も大きな消費者の選好変化が生じるのが CNG 車へのシフトであり 年におけるエネルギー需要では全体の 8% を占める 年における本シナリオのエネルギー需要は 相対的に燃費性能の優れた CNG の割合が増えることから BAU と比較して 2.5% 減の 1,843 PJ となる ( 図 3-5) 41

43 PJ 2,000 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 3% 3% 4% 4% 6% 8% 42% 41% 39% 39% 39% 55% 56% 56% 51% 49% 電気 LPG CNG ディーゼル ガソリン 図 3-5 燃料別乗用車エネルギー需要の見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合 ( 右図 ) シナリオ 1.2: ガソリン価格がディーゼル価格よりも 35% 高価になった場合シナリオ 1.2 ではシナリオ 1.1 と比較して ガソリン車から CNG 車への選好がより高まるアンケート結果を反映し エネルギー需要でも CNG の占める割合が 17% へと大きく拡大する ( 図 3-6) シナリオ 1.1 同様 相対的な燃費水準の良い CNG の割合が増えるため 年時点での乗用車エネルギー需要は BAU 比 7% 減の 1,758 PJ に達する PJ 2,000 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 3% 4% 5% 7% 12% 17% 42% 41% 40% 42% 42% 55% 56% 54% 41% 34% 電気 LPG CNG ディーゼル ガソリン 図 3-6 燃料別乗用車エネルギー需要の見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合 ( 右図 ) シナリオ 1.3: ガソリン価格がディーゼル価格よりも 50% 高価になった場合シナリオ 1.3 ではシナリオ 1.2 と比較して ガソリン車から CNG 車へのシフトは大きな変化はないとするアンケート結果を反映し エネルギー需要でも CNG の全体に占める割合は 17% とシナリオ 1.2 より微増するに留まる ( 図 3-7) エネルギー需要では 年において BAU と比較して 7.67% 減の 1,745 PJ となる 42

44 PJ 2,000 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 3% 4% 5% 7% 12% 17% 42% 41% 40% 42% 43% 55% 56% 53% 40% 33% 電気 LPG CNG ディーゼルガソリン 図 3-7 燃料別乗用車エネルギー需要の見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合 ( 右図 ) シナリオ 2.1: ディーゼル価格がガソリン価格と同水準になった場合シナリオ 2.1 では消費者のディーゼル車に対する選好が低くなるアンケート結果を反映し これを大きく代替するガソリン車のエネルギー需要に占める割合が 年で 64% と 年の 55% から増加する 乗用車の総エネルギー需要では ディーゼル車と比較して相対的に燃費の良いガソリン車の割合が増加することから 年時点で BAU 比 2.46% 減の 1,844 PJ に達する PJ 2,000 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 2% 2% 2% 4% 5% 42% 41% 37% 32% 29% 55% 56% 58% 62% 64% 電気 LPG CNG ディーゼルガソリン 図 3-8 燃料別乗用車エネルギー需要の見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合 ( 右図 ) シナリオ 2.2: ディーゼル価格がガソリン価格よりも 25% 高価になった場合シナリオ 2.2 ではガソリン需要の占める割合は 年時点で 67% へと増加する一方 ディーゼルの割合は同 22% へと縮小する 相対的に価格が安い CNG の割合は 年で 8% へと拡大する 乗用車のエネルギー需要は 年において BAU 比 5.24% 減の 1,791 PJ に達する 43

45 PJ 2,000 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 3% 3% 3% 6% 8% 42% 41% 36% 27% 22% 55% 56% 58% 64% 67% 電気 LPG CNG ディーゼルガソリン 図 3-9 燃料別乗用車エネルギー需要の見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合 ( 右図 ) シナリオ 2.3: ディーゼル価格がガソリン価格よりも 50% 高価になった場合シナリオ 2.3 ではガソリン需要の全体に占める割合が 年の 60% から 年の 68% へと増加する一方で ディーゼルの割合は 年で 21% へと低下 他方 CNG の割合は 8% へと増加する BAU と比較して本シナリオの 年における乗用車エネルギー需要は 6.56% 減の 1,766 PJ となる PJ 2,000 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 3% 3% 3% 3% 6% 8% 42% 41% 36% 27% 21% 55% 56% 58% 64% 68% 電気 LPG CNG ディーゼルガソリン 図 3-10 燃料別乗用車エネルギー需要の見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合 ( 右図 ) シナリオ 3.1:CNG 価格がディーゼル価格と同水準になった場合これまでのシナリオではガソリンのディーゼルに対する相対的な価格水準 及びディーゼルのガソリンに対する相対的な価格水準を見てきたが シナリオ 3.1 では CNG 価格がディーゼル価格と同水準となった場合を想定 消費者の選好変化を分析した 本シナリオでは CNG の価格優位性が保たれないため 年時点での乗用車エネルギー需要に占める割合も 3% に留まる 年時点での乗用車エネルギー需要は BAU と比較して 0.46% 増の 1,899 PJ となる 44

46 PJ 2,000 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 2% 2% 2% 42% 41% 38% 37% 35% 55% 56% 57% 60% 62% 電気 LPG CNG ディーゼルガソリン 図 3-11 燃料別乗用車エネルギー需要の見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合 ( 右図 ) シナリオ 3.2:CNG 価格がガソリン価格と同水準になった場合シナリオ 3.2 でもシナリオ 3.1 と同様に CNG のガソリンに対する価格優位性が維持されないため その乗用車エネルギー需要に占める割合も 年で 2% に留まる 年時点での乗用車エネルギー需要は 1,903 PJ となる (BAU 比 0.7% 増 ) PJ 2,000 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 2% 2% 1% 2% 1% 42% 41% 39% 37% 36% 55% 56% 57% 60% 62% 電気 LPG CNG ディーゼルガソリン 図 3-12 燃料別乗用車エネルギー需要の見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合 ( 右図 ) シナリオ 3.3:CNG 価格がガソリン価格よりも 25% 高価になった場合シナリオ 同様 シナリオ 3.3 においても CNG 価格の他燃料価格への優位性が保たれないため 需要も伸びず全体に占める割合としても 年時点で 2% に留まる 年時点での乗用車エネルギー需要は 1,899 PJ であり これは BAU と比較すると 0.48% 増の水準である 45

47 PJ 2,000 1,800 1,600 1,400 1,200 1, 電気 LPG CNG ディーゼルガソリン % 2% 2% 2% 1% 2% 1% 42% 41% 39% 37% 36% 55% 56% 57% 60% 62% 電気 LPG CNG ディーゼルガソリン 図 3-13 燃料別乗用車エネルギー需要の見通し ( 左図 ) 燃料別乗用車エネルギー需要の割合 ( 右図 ) 3.3. シナリオ別乗用車エネルギー需要見通し比較シナリオ別の乗用車エネルギー需要見通しを図 3-14 図 3-15 に比較する 図が示す通り 車種別選好の変化に応じ BAU と比較し 年時点での省エネルギー効果が期待できる 本分析で対象とした車種の中で 想定される燃費が最も悪いディーセル車の割合が小さくなるシナリオ 1.3 では BAU と比較して 年時点での省エネルギー効果が 7.7% に推計される PJ 2,000 1,800 1,600 1,400 1,200 1, BAU シナリオ1 シナリオ2 シナリオ3 シナリオ4 シナリオ5 シナリオ6 シナリオ7 シナリオ8 シナリオ9 図 3-14 シナリオ別乗用車エネルギー需要見通しの比較 ( 年 ~ 年 ) 46

48 PJ 1,950 1,900 1,850 1,800 1,750 1,700 1,650 1,890 1,843 1,758 1,745 1,844 1,791 1,766 1,899 1,904 1,899 図 3-15 シナリオ別乗用車エネルギー需要見通しの比較 ( 年 ) 3.4. 政策への示唆 年には 乗用車保有台数が現状から 5 倍となる 8,000 万台に達する見通しである このため インドにおいて その燃料選択は供給から消費 さらにはその結果としての CO2 排出等 様々なインプリケーションを有する 具体的には 燃料の選択は供給段階において 原油輸入の増加 国内石油精製施設の拡充 天然ガスパイプライン等のインフラ形成に対する大きな影響をもつ 同時に消費の結果として引き起こされる地域ならびに地球環境への影響ついて大きな示唆を持つ そこで ここまでのモデル推計によるシナリオ分析を基に得られた 主に省エネ政策への示唆を以下に集約する 1. 消費者の燃料価格の車種変更に対する弾力性の高さ 省エネルギーポテンシャル インドの消費者は 新車購入時の車種決定において 燃料価格に弾力的に反応することが明らかとなった 具体的には 新車の車種決定要因として燃料価格を重視する傾向にあると指摘できる シナリオ分析が提示する通り ガソリンならびに軽油の相対価格変化によって 消費者は新車購入に際してガソリン車やディーゼル車から CNG 車へ大きくシフトする見通しである 特に 著しく CNG 車へのシフトが進む見通しを提示したのは ガソリン価格がディーゼル価格よりも相対的に 35% 以上高価になった場合である 同様にディーゼル価格がガソリン価格よりも 25% 高価となった場合 ディーゼル車から CNG 車へのシフトが進む 燃料価格の変化による車種変更の弾力性の高さは 低価格で CNG 供給が行われているためである 今回のシナリオ分析では想定していないが 低燃費車 47

49 へのシフトを政策目標とする場合 初期投資コストを補助金支給等で行うことによってそのシフトを促進するポテンシャルを示唆するものである 2. エネルギー供給インフラ整備の必要性 分析から明らかな通り 燃料価格政策の変化は消費者の車種選好に大きく影響を与える このため 燃料別のエネルギー需要構成への変化に対するインフラ整備への影響も指摘できる 将来にわたる具体的なエネルギー供給見通しを描いていない場合 需要に牽引される形でのインフラ形成がなされ エネルギーセキュリティや環境対策のための政策手段が限られてしまう可能性がある 将来的な国内原油生産ならびに天然ガス生産の見通しを踏まえ 輸入確保ならびに国内供給インフラ形成など 統合的なアプローチから政策形成ならびに適切なインフラ形成計画を実現することが必要となる 48

50 4. 鉄道 4.1. 概況インドの鉄道は 大英帝国が植民地としてインドを統治していた時代に大部分が敷設された 1947 年に独立した後 パキスタンの分離独立に伴う印パ国境地域を中心とする鉄道網の再編以外に大々的な増設は行われていない このため 過去 60 年間の総延長の増加は 2 割程度に留まっている 現在 インドの鉄道網は 鉄道省とその管轄下にあるインド国鉄により運営されている インド国鉄が保有する車両のうちディーゼル車両が全体の 5 割を占めているが 今後は各路線の電化が進められていく予定である しかし 鉄道インフラの老朽化が深刻であり 設備更新が急がれている 貨物輸送については かつてはインドの貨物需要の大部分を占めていたが 現在のシェアは 3 割前後にとどまっている インド国鉄としては 少なくとも 5 割にすることを目標としている 主な貨物は石炭 鉄鉱石 セメントなどである 一方で 旅客輸送は 近年急速に増加している ただし 運賃は政策的に低く抑えられており インド国鉄の財政を圧迫する一因となっている 2014 年 7 月の政権交代で誕生したモディ政権は 何年も先送りにされてきた鉄道の運賃改定に乗り出すと報道されている 国鉄以外に 大都市では 急激に増加する旅客需要に対応するために地下鉄 ( メトロ ) の整備が急ピッチで進められている 既に カルカッタ チェンナイ デリー ムンバイ バンガロール グルガーオンで営業運転を開始しており 他の都市でも建設中 計画中のものが多数ある そして インド国鉄は長距離高速鉄道を計画中であり 年連邦予算にも関連予算が盛り込まれた 日本をはじめ フランスや中国がプロジェクトの獲得を目指している 4.2. 所管官庁及び関連企業インドの鉄道網は 鉄道省 (Ministry of Railways) 傘下の国鉄 (Indian Railways) が運営している 図 4-1 は インド国鉄の組織体制の概略である 鉄道大臣の下に鉄道委員会 (Railway Board) が設置され インドの鉄道政策の意思決定をおこなっている この下に 16 の地域に分割された地域会社と国鉄が運営するカルカッタメトロが位置付けられている インドの鉄道網と 17 ブロックの区分を図 4-2 に示す また インド国鉄は車両の生産部門を有している その他に 乗務員を養成するための教育機関や研究開発部門 さらにインド高速鉄道会社等の公営企業がある 49

51 鉄道大臣 鉄道副大臣 鉄道委員会 各地域の鉄道 1. 中央鉄道 2. 東部中央鉄道 3. 東海岸鉄道 4. 東武鉄道 5. 北部中央鉄道 6. 北東部鉄道 7. 北西部鉄道 8. 北東部辺境鉄道 9. 北部鉄道 10. 南部中央鉄道 11. 南東部中央鉄道 12. 南東部鉄道 13. 南西部鉄道 14. 南部鉄道 15. 西部中央鉄道 16. 西部鉄道 17. カルカッタメトロ 生産部門 Chittaranjan 機関車製作所 ディーゼル機関車製作所 旅客車両工場 鉄道車両工場 鉄道車輪工場 その他 中央鉄道電化機構 中央車庫近代化機構 インド国鉄プロジェクトマネジメントユニット インド国鉄代替燃料機構 インド国鉄大学校 公営企業 インド高速鉄道会社 RITES 等 図 4-1 インド国鉄組織図 出典 : 鉄道省資料からエネ研作成 図 4-2 インドの鉄道網及び 17 のブロック 出典 : 50

52 インドでは 国鉄が運営するカルカッタメトロ以外に 5 つの大都市圏でメトロが営業運転をおこなっており これらの運営は国鉄ではなく各メトロの運営会社がおこなっている さらに 7 都市でメトロの建設が進められており 17 都市でメトロの建設が計画されている 表 4-1 に インド国内のメトロ一覧を示す こうしたインド国内でのメトロの建設のうち カルカッタ チェンナイ ムンバイ バンガロール デリーに JICA が協力している 表 4-1 インドのメトロ一覧状況都市営業中カルカッタ チェンナイ デリー ムンバイ バンガロール グルガーオン建設中ジャイプール チェンナイ ハイデラバード ナビ ムンバイ コチ ラクナウ アーメダバード=ガンディナガー計画中ボパル ブバネーシュワル チャンディーガル インドール カンプール ルディヤーナー ナーグプル ナシク パンタ プネー スーラト スリナガー ヴィジャヤワダ ヴィシャーカパトナム ムンバイ グワーハーティー デリー首都圏 出典 :Indian Railways Statistical Publication インド国鉄の概要インド国鉄は毎年統計年鑑を公表している 表 4-2 は直近 10 年間のインド国鉄の総延長 車両数 運賃収入等である これらのデータはインド国鉄が管理する全てのデータが含まれているが 地域ごとのデータは公開されていない インド国鉄の路線の総延長は 1950 年時点で 53,596 キロメートル敷設されており 過去 60 年間で 1 万 2 千キロメートル延伸され 65,436 キロメートルとなっている 直近 10 年でみると 2,215 キロメートル延伸されており 継続的に延伸が進められていることがわかる 運用されている機関車を種別ごとに整理したものを図 4-3 に示す インド国鉄は主要路線の電化を進めており 直近では約 30% が電化されている このため 路線が拡大する中で 相対的にディーゼル機関車の増加よりも電気機関車の増加が大きい 2012 年時点で 5,345 両のディーゼル機関車 4568 両の電気機関車が運用されており さらに 43 両の蒸気機関車も運用されている 51

53 図 4-4 は旅客需要と旅客運賃収入の推移である インドの旅客需要は年々増加し続けており この 10 年で旅客需要が 2 倍に拡大している 一方で 旅客運賃は 政策的に低く設定されており 旅客需要に対する旅客運賃収入の伸びが低く 毎年の旅客運賃収入の変動も大きい 図 4-5 は貨物需要と貨物運賃収入の推移である 貨物需要は経済成長を背景として堅調であり 過去 10 年間で 1.7 倍に増加した これにあわせて貨物運賃収入も増加しており 特に 2012 年 -13 年に運賃を改定したことで 2003 年 -04 年と比較すると貨物運賃収入が 3 倍に増加している 図 4-6 は 2012 年 -13 年の貨物輸送の内訳である 図が示す通り 約 50% が石炭であり これはインドの主要な電源である石炭火力発電所向けの発電用石炭と鉄鋼部門向けのコークスである 次いで 鉄鉱石 セメントなどが約 10% を占めている したがって インド国鉄が取り扱う貨物の大部分は原材料で占められており 貨物運賃の値上げは 重工業部門だけでなく ほぼすべての部門の費用を押し上げることになることがわかる 一方で 鉄道の近代化や改修のために必要な資金を調達するために ある程度確実に回収可能な貨物運賃に偏っているともいえる こうした点は 図 4-4 図 4-5 に示したように インド国鉄の主要な運賃収入源が貨物であることからもわかる 2012 年 -13 年の時点で 運賃収入の内 6% が旅客 残り 94% が貨物である これは 旅客運賃が低く設定されているため これによる赤字を貨物運賃収入で賄っていることが一因となっている また こうした構造によって 鉄道インフラへの投資が滞っている 図 4-7 は 軽油消費量と電力消費量の推移である 直近 10 年で 軽油消費量は 31% 電力消費量は電化が進んだことで 46% 増加している 52

54 表 4-2 インド国鉄の概要 年度 総延長 ( キロメートル ) 63,221 63,465 63,332 63,327 63,273 64,015 63,974 64,460 64, 蒸気機関車 車両数 ディーゼル機関車 4,769 4,807 4,793 4,816 4,843 4,963 5,022 5,137 5, 電気機関車 3,004 3,065 3,188 3,294 3,443 3,586 3,825 4,033 4, 旅客数 ( 単位 : 百万人 ) 5,112 5,378 5,725 6,219 6,524 6,920 7,246 7,651 8, 交通量エネルギー消費量運賃収入 旅客交通量 ( 単位 : 百万人 km) 541, , , , , , , ,508 1,046, 貨物交通量 ( 単位 : 百万トン km) 石炭 ( 単位 千トン ) ディーゼル 2,060,396 ( 単位 : キロリットル ) 2,080,634 2,111,190 2,211,531 2,284,061 2,260,754 2,400, ,699,616 電力 ( 単位 : 百万 kwh) 9, , , , , , , , , , 旅客収入 ( 単位 : 千万ルピー ) 13, , , , , , , , , , 貨物収入 ( 単位 : 千万ルピー ) 27, , , , , , , , , , 出典 :Indian Railways Statistical Publication

55 蒸気機関車ディーゼル機関車電気機関車 車輌数 ( 両 ) ,769 4,807 4,793 4,816 4,843 3,443 3,004 3,065 3,188 3,294 4,963 5,022 3,586 3,825 5,137 5,197 4,033 4, 図 4-3 蒸気機関車 ディーゼル機関車 電気機関車の車両数 出典 :Indian Railways Statistical Publication ,200 5,543 5,656 5,349 6,000 1,000 4,903 4,718 4,941 5,000 旅客交通量 (10 億人キロ ) ,387 3,199 3,668 4,247 4,000 3,000 2,000 旅客輸送収入 ( 千万ルピー ) 200 1, 出典 :Indian Railways Statistical Publication 図 4-4 旅客交通量及び旅客収入 54

56 1,200 83,479 90,000 1, ,744 60,687 56,912 51,749 46,425 41,073 35,535 27,403 30,489 80,000 70,000 60,000 50,000 40,000 30,000 20,000 10, 貨物交通量 ( 百万トン km) 貨物収入 ( 千万ルピー ) 出典 :Indian Railways Statistical Publication 図 4-5 貨物交通量及び貨物収入 肥料, 4.6% その他, 12.2% 原油, 4.0% セメント, 10.5% 石炭, 49.2% 鉄鉱石, 11.1% 鉄鋼, 3.5% 穀物, 4.9% 出典 :Indian Railways Statistical Publication 図 4-6 貨物輸送量内訳 ( 年 ) 55

57 軽油消費量 電力消費量 = 図 4-7 軽油消費量と電力消費量の推移 ( = 100) 出典 :Indian Railways Statistical Publication インド国鉄の省エネ等の取組インド国鉄は急激に増加する輸送需要に対して 路線の拡張や容量の増加に取り組んでいる 同時にエネルギー消費量が急激に増加しており 図 4-7 に示したように 過去 10 年間のトレンドから考えれば 将来的にエネルギー消費量が増加し続けると考えられる このため エネルギー効率を改善する目的で 運転や整備等の自動化技術の開発 IT の活用した効率化に取り組んでいる また 単一の機関車による運行ではなく 出力の小さい複数機関車による運行に切り替えることでエネルギー効率を改善 編成の長大化 運行スケジュールの効率化等 運用面でも取組を進めている しかし 増加し続ける輸送需要への対応とインフラの近代化等が優先され インド国鉄の中で省エネへの取組は低調である また インドは鉄道省と国鉄が一体であるため 規制官庁による省エネルギー政策の推進というよりも 事業者の自主的な努力として省エネルギー施策が展開されている このため 現在行われている省エネ関連の取組がどの程度実施されているのか 実効性に課題が残る 省エネと同様に 消費するエネルギーを代替するために 太陽光エネルギーとバイオ燃料の導入が推進されている 太陽光パネルを駅舎や車庫といったインド国鉄所有建物の屋上に設置することが計画されている また バイオ燃料については ディーゼルとの混合率を 5% に引き上げることを目標としている 56

58 こうした状況の中 UNDP と GEF が資金を拠出し インドの鉄道省や電力省が鉄道部門でのエネルギー効率改善のためのプロジェクト 3 を 2011 年 9 月から開始している この計画では 鉄道部門でのエネルギー効率を改善するために エネルギー管理システムの導入や太陽光発電システムの導入 及び関連する技術の紹介などを予定している 4.5. 新政権の鉄道政策インド国鉄はこれまで国営の鉄道事業者として 営利のための鉄道運営よりも低所得者層向けの福祉という性格を持った経営を行ってきたため 効率性よりも公益性が優先されてきた 一方で 2014 年 7 月に就任したモディ首相は インフラとしての鉄道の充実のため 収入面では適正な運賃設定を原則とし 支出の面では直接投資 (FDI) と官民連携プロジェクト (Public Private Partnership) の活用によるインド国鉄の運営を推進していく意向である 貨物これまで 鉄道による貨物輸送は インドの貨物輸送シェアの 50% ほどを占めていたが 近年はシェアが低下し 30% 程度となっている この理由として 特に 4 大都市を結ぶ主要路線において線路容量がひっ迫していることが挙げられる 貨物は旅客よりも速度が遅く かつ旅客優先のため旅客の追い越し待ちをしなくてはならない こうした状況の中 旅客 貨物それぞれに最適なダイヤや運行が難しい状況が常態化している したがって 貨物の到着時間の見通しが立てられず 原材料のような一次産品以外はトラック輸送に移行したためである 一方で 鉄道輸送は環境面で注目されている 特に気候変動対策として大量の物資を少ないエネルギーで輸送することができる点で 鉄道輸送はトラック輸送よりも優れている そこで トラックによる道路輸送から 鉄道による集合運搬にモーダルシフトを行うことで交通部門のエネルギー効率を改善することを目指した政策が検討されている 具体的な施策として 年連邦予算には主に以下の項目が盛り込まれた 石炭輸送インフラ開発の迅速化により 1 億トンの輸送需要拡大 官民連携による物流センター及び海上交通とつなぐ港の建設を通じた他の輸送手段とのインターフェースの向上 試験的な空き車両の活用システムの構築 業界団体との連携による野菜と果物の輸送量の増加 牛乳用タンカーの建造 4 3 Improving Energy Efficiency in the Indian Railways System ing_energyefficiencyintheindianrailwaysystem.html

59 他にも第 12 次五カ年計画では コンテナ化の推進による貨物の積み替えの迅速化や大型車両の建造やこれまでよりも大きな重量を支えられる車輪の導入を目指している さらに 旅客と貨物双方の輸送量を増加させるためにはまず旅客輸送と貨物輸送を分離する必要がある このため 最も交通量の多い路線から優先的に貨物専用回廊 (Dedicated Freight Corridor) を建設する予定である 年連邦予算で デリーとムンバイをつなぐ西部貨物専用回廊とデリーとコルカタをつなぐ東部貨物専用回廊が承認された 旅客旅客鉄道は インド国鉄が低所得者層向けの福祉として機能している一面として 運賃が低く抑えられていることで 多くの人々の長距離移動の手段となっていることが挙げられる ただし 貨物と同様に ダイヤ通りに運行されておらず 遅延が多発している 一方で インド国鉄では バス等の道路交通や空路と対抗できるよう旅客の高速化が計画されている これは時速 160~200km を目指す既存路線の高速化と 時速 300km 超の新規路線からなる高速鉄道の 2 通りの方法が検討されている 現在 以下の既存路線の準高速化 (160km/h~200km/h) を計画中である デリー =アグラ チェンナイ=ハイデラバード デリー =チャンディーガル デリー =カンプール ムンバイ=アーメダバード ムンバイ=ゴア マイソール=バンガロール=チェンナイ ナーグプル=ラーイプル=ビラ スプル ナーグプル=シカンダラーバード これらのうちデリー =アグラ間の Gatimaan Express が 2014 年 11 月に開始予定であったが 鉄道安全委員会の許可が下りず 未だ運行開始できていない その他の路線については 年の連邦予算で予算が承認されている 時速 300km を超える高速鉄道について これを建設するために長期間にわたって検討されてきた 長い検討期間を経て 2009 年にインド国鉄は 鉄道ビジョン 2020 を発表し 計画を具体化する 6 路線を発表した このうち ムンバイ=アーメダバード間の路線についてフランスの Systra 社とインドの RITES 社 ( インド国鉄の子会社 ) によってプレフィージビリティースタディーが実施されている また 2013 年からは JICA によりより詳細な建設計画の内容についてフィージビリティースタディーを行っている 調査結果は 2015 年 5 月に発表される予定である 58

60 2014 年に入り 7 月にインド鉄道相がインド高速鉄道の最初の区間として ムンバイ= アーメダバード高速鉄道回廊を建設する意向を表明した 費用は 6 千億ルピーとの試算がなされているため 対内直接投資と官民連携型 (Public Private Partnership: PPP) も併せて利用することで資金確保を目指している 同計画に関連して 年の連邦予算のなかで 初期費用として 10 億ルピーが承認された 最終的には デリー ムンバイ カルカッタ チェンナイを高速鉄道でつなぐ Diamond Quadrilateral Network の建設を目指している 現在 日本 中国そしてフランスがインド高速鉄道への参入を目指している 遠隔地 北東部及びアンドラ プラデシュ州とテランガーナ州の開発長大な路線網が敷設されているインドにあって 鉄道インフラの発展が遅れている地域の開発が急がれている 特に 北東部 ( バングラデシュ ブータン ミャンマーそして中国に囲まれている地域 ) やデカン高原とその周辺に位置するアンドラ プラデシュ州と 2014 年 6 月にアンドラ プラデシュ州から独立したテランガーナ州の開発に重点的に資源を割いていくことが予定されている 4.6. 鉄道部門の政策課題 国鉄運営インド国鉄は 公益的な側面をもつ国営鉄道事業者であるが 近年はその非効率性が指摘され 改革の必要性が検討されている インド国鉄は 運賃収入 政府からの借り入れ 民間金融機関からの借り入れの 3 つの収入で運営されている しかし 現在の運賃収入は十分な水準ではなく 政府からの借り入れは返済できない状況にあり 民間からの借り入れは利子のみを返済する状況である このため インド国鉄は恒常的な赤字経営ではあるが 公益的な側面からそれが常態化している インドにおいて鉄道の旅客輸送は公共の福祉として安価な交通手段を提供するサービスとして位置付けられているため 収益を改善するために運賃改定が急務となっているが 値上げは政治的に機微な課題である しかし インド国鉄の旅客運賃の水準では運航費用の 7 割程度しか運賃を回収できておらず 年は旅客部門で 2,200 億ルピーの赤字となった 5 このため 旅客部門の赤字を埋め合わせるために 貨物運賃が高額に設定されている 運賃の改定について 前政権では支持率維持のために 運賃を低く抑えてきたが 新たに誕生したモディ政権では運賃を 14.2% 上げる決定をした 6 ただし この値上げ水準でも抜本的な収支改善に必要な水準にはほど遠い状況である 現状の運賃水準は 旅客輸送を増やした分だけ赤字を計上する構造になっているため 抜本的な収益構造の改革なしには輸送量の増加に対応するための投資を回収することは不可能である 5 12 th Five-year Plan, pp

61 さらに 収入面だけでなく 世界中どこの国鉄でも同じ課題に直面しているように 人件費 ( 給料及び年金 ) がインド国鉄の支出の 50% を占めている インド国鉄は 135 万人を雇用する巨大企業であるが 収益を改善するために人員を整理することは 雇用の確保という公共の要請により これを削減することが難しい さらに 大量の従業員を抱えているため これを支持層としている政治家の存在や強力な労働組合といった障害が存在している そして 最大の課題は 鉄道省が規制官庁であるとともに 鉄道の運営事業者でもあるため 規制を立案する組織として機能することが難しい点である 規制官庁である鉄道省とインド国鉄を分離することが課題とされており モディ首相はそれに取り組む意向を示している 省エネルギーに関する課題インド国鉄の支出に占める燃料費の割合は約 2 割と非常に大きな割合を占めている このため 燃料費を削減するためにエネルギー転換や省エネに取り組んでいる 路線の電化を進めることで 割高な軽油から安価な電力にシフトが進められている ただし 鉄道省内では 国全体では省エネにならないとする意見もある インドでは常に電力が不足しており 鉄道が電力使用量を増加させると グリッドから電力供給を受けられなくなった家庭や事業者が ディーゼル自家発電機を運転する必要に迫られる こうした発電機はディーゼル機関車よりも効率が低いため ディーゼルの使用が国鉄からそれ以外の自家発電に切り替わることで 結果としてより多くの軽油を消費することにつながる このため インド国鉄がディーゼル機関車を使い続けた方が インドの国全体での省エネルギーにつながるという意見がある また インド国鉄は省エネルギーのためにいくつかの施策を実施している しかし どの施策が どれだけエネルギー効率改善に寄与したかという点が把握されていない さらに どういったところでエネルギーが浪費されているかという点を詳細に把握していないため 省エネルギー施策を行うことが難しい状況にある したがって 現在のエネルギー消費実態について細かな分析が課題となっている そして インド国鉄について インドの運輸部門における位置付けが 国の方向性として必ずしも明確となっていない 鉄道は 貨物 旅客ともドアツードアの輸送ができないことが弱点であり 他の交通手段との連携が不可欠となる つまり 統合的な交通政策において 都市内の短距離輸送 都市間の長距離輸送等の明確な位置付けが必要となる 例えば 旅客輸送においては メトロが各地で建設されているが 最寄駅から目的地までの接続 (Last-mile connectivity) のための交通手段を検討する必要がある 貨物輸送には 他の輸送手段 ( トラック 船舶 飛行機 ) との貨物の積み替えを円滑に行うための物流ハブの建設が必要である また こうした他の交通手段との連携は複数の省庁や事業者との調整が必要である 60

62 PAT 制度の可能性 (Perform, Achieve and Trade) BEE はPAT と呼ばれる産業部門のエネルギー消費削減ベンチマークの設定とベンチマーク以上の省エネルギーを達成した事業者は超過分を他の業者に売却できる制度を推進している 現在 BEE 内では これをインド国鉄に適用し 17 の区画ごとに目標値を設定し 区画間で超過達成分を取引できる制度を検討中である ただし インド国鉄はこれに消極的で インド国鉄は鉄道部門を独占しているため PAT は成り立たないとしている また インド政府は省庁間の調整に極めて消極的である性質があるため BEE とインド国鉄との調整は難航することが予想される 61

63 5. ワークショップ開催概要 2015 年 1 月 28 日に 本共同研究の成果を共有するためのワークショップをグジャラート州の PDPU で開催した 当日のプログラムは 別添えを参照されたい ワークショップでは 弊所から本プロジェクトに関する紹介をした上で 簡潔に日本の運輸部門での成功について報告した 続いて 今年度共同研究を行った PDPU と TERI からそれぞれ研究成果について報告された PDPU の Pramod Paliwal 教授から 燃料価格政策や燃費規制 排ガス規制について関連する文献調査の結果から これらの政策のこれまでの経緯や方向性 及び市場調査の際に含意について報告があった 続いて Hemant Trivedi 教授からグジャラート州の二輪及び四輪保有者を対象とした燃料価格や省エネに関する市場調査結果について報告された 次に TERI の Sarbojit Pal 氏から 市場調査結果を活用し 2030 年台の自動車の燃料消費量の見通しについて報告された また インドの自動車市場において ガソリン 灯油 CNG LPG の燃料価格の水準が重要な要因となっており これらの価格水準が変化した場合の自動車市場への影響について試算した結果が報告された 次に 燃料供給事業者の視点から 国営石油販売会社 HPCL(Hindustan Petroleum Corporation Limited) の Arvind Govil 氏から ディーゼルへの補助金撤廃前後の市場の反応について報告された 燃料販売データでは補助金撤廃の影響はなく 一方でこれまでの補助金によりインドの乗用車市場のディーゼル化が進行していると指摘し 軽油の販売量が増加傾向にあることを示した こうした点も踏まえ ディーゼルの効率的利用を促進するために 燃料価格に関連する制度の統合等を検討する必要があると述べた 続いて 国営石油会社 IOCL(Indian Oil Corporation Limited) の Mahesh C. Gupta 氏から 同社の製油所での省エネの取組や 今後の排ガス規制に対応した製油設備の改修等について報告があった そして WIAA(Western India Automobile Association) の Shrinivas Desai 氏から 運輸事業者等の消費者の視点から運輸部門での省エネについて報告があった 同氏は WIAA での運転トレーニング講習の概要について説明したうえで こうしたドライバーのトレーニングの一環として トラックを運転する時の省エネドライブを教えることの重要性が指摘された これは 多くのトラックのドライバーが 安全運転や燃料消費量を意識せずに運転しており 教育や啓発を継続的に進めていくことが重要であると指摘した 次に 政府関連機関から 現在のインドにおける省エネに関連する取組について報告があった まず PCRA(Petroleum Conservation Research Association) の Sumant Kumar 氏から 日本の ECCJ( 省エネルギーセンター ) と共同で実施しているエコドライブの講習の概要について発表し これまで 12,000 人のドライバーを対象として講習を実施 平均で 10% 程度のエネルギー効率の改善につながっていることが報告された こうした取組を踏まえ エコドライブ講習を拡大し ドライバーへの教育と啓発を継続的に実施していくことで 行動を変化させることができると指摘した 続いて BEE(Bureau of Energy Efficiency) の Saurabh Diddi 氏から インドの運輸部門での省エネ政策について報告があった 同氏 62

64 は 2005 年から検討してきた乗用車の燃費基準を 2014 年 1 月に発表 2017 年から規制を開始すると述べたうえで 今後は重量車の燃費基準の策定について PCRA と協力して調査 研究を進めていると述べた ただし 重量車の燃費基準について 実際の燃料消費状況について貨物や運航状況によって千差万別であり データの確保と分析が課題となっていると指摘した また 燃費改善のための技術のロードマップについても検討を進めていると述べた これらの発表を踏まえ 参加者との議論をおこなった その際に 共同研究を踏まえた政策提言案を示し議論をおこなった 提言案について 燃料価格政策について ステークホルダーが投資を決定する際に参照する要因の一つでありある程度の見通しが立てられるような予測可能性が重要であるとの意見があった また 燃費性能に優れる乗用車の普及促進について BEE からインセンティブの付与に対して肯定的な意見が述べられたが 制度設計のためのより詳細な検討が必要となると指摘された そして 政策提言案の中で車検制度のような定期的なメンテナンスについても省エネの観点から重要との指摘があった 図 5-1 ワークショップ写真 63

65 6. 政策提言今後の経済成長によりエネルギー消費量の急激な増加が見込まれるインドの運輸部門において 燃費性能に優れる乗用車の普及のために Pandit Deendayal Petroleum University(PDPU) 及び The Energy and Resources Institute(TERI) とエネルギーの節約と効率改善についての次のような共同研究を行った 政府機関 自動車メーカー エネルギー供給事業者へのヒアリング グジャラート州において燃料価格や省エネに関するアンケート調査 運輸部門に特化した計量経済モデルを用いて 運輸部門の省エネポテンシャルを推計 これらの共同研究結果 短期的に自動車保有者の行動を変化させるための啓蒙活動の強化 中期的に燃費性能に優れた乗用車を普及させていくためのインセンティブ制度の設計 そして長期的には燃料価格制度や燃費規制 排ガス規制の統合による税制や関連する制度のグリーン化が重要である 短期的な啓蒙活動の強化ステークホルダーへのヒアリングやアンケート調査を通じて インドの自動車保有者が燃費の改善に関心を示していることが明らかとなった しかし 燃費改善のための情報へのアクセスが限られており これを改善することはエネルギーを節約するための第一歩である また インドは乗用車のライセンス制度があるが エコドライブの促進など運転者の行動を変えていくための教育カリキュラムは整備されていない さらに インドの自動車メーカーは自主的にドライビングスクールを開校しているが 全ての運転者に対応できる体制とはなっていない そこで こうした点を踏まえ 以下を提案する 1. メーカーとの共同でのエコドライブの促進運動 エコドライブコンテストの実施 公的部門による啓蒙活動だけでなく 乗用車を販売するメーカーと協力することで 燃費改善のための運転方法や燃費性能に優れた乗用車に触れる機会を提供することが重要である こうした取り組みを継続していくことは 乗用車の使用段階での燃料消費量の削減に貢献でき 維持費用に敏感なインドの消費者に燃費性能に優れた乗用車をアピールすることができる アンケート調査の結果 多くの自動車保有者が 3 カ月に一度の割合で何らかのメンテナンスを行っていることが明らかとなった この結果は重要であり 自動車保有者がメンテナンスの機会に 燃費改善のための方法について情報に触れるよい機会となり得る そこ 64

66 で この点を踏まえ以下を提案する 2. 車検制度及び車検を受けるためのインセンティブ付与 定期的な乗用車のメンテナンスを受けることにインセンティブを付与することで 燃費改善に関する情報を提供する機会を創出することができる 例えば 定期的な車検制度を導入することで こうした機会を政策的に創出できる 中期的に必要となる政策措置市場調査の結果から 自動車の保有者は購入段階 使用段階を通してコストに非常に敏感であることが定量的に示された したがって 燃費性能に優れた乗用車を普及させる観点から 何らかのインセンティブを導入することで そうした乗用車の普及を後押しすることができる 具体的には 以下の政策措置を提示する 3. 車体登録時の登録料の減免措置 インドでは乗用車の購入後に登録料を一括して支払うことで登録される この際の登録料には 燃費性能などが考慮されていない 燃費性能に優れた乗用車の普及を促進していくためには 車体登録時の登録料を減免することが非常に重要である 4. 燃費性能に優れた乗用車に対するインセンティブの付与 インドは 年から燃費基準が導入される 同時に 5 段階評価によるラベル制度の導入を準備している こうした制度で定義される燃費性能に優れた乗用車の普及を促進していくために 補助金の導入が重要である 5. 旧型車への買い換えインセンティブ インドは 初回登録があるのみで その後の乗用車の使用状況については統計が存在しない ( 初回登録後 15 年 5 年 5 年ごとに登録料の支払いが必要 ) また 一部地域では大気汚染対策として車齢 15 年以上の乗用車を排除する制度が導入されているが 実施に課題がある インドでは燃費性能の低い乗用車が継続的に使用され 大量の燃料を消費している こうした乗用車の入れ替えを促進するためには旧型車の買い換えを促進するためのインセンティブが必要である 例えば 初回登録時の書類に基づき 15 年経過した乗用車をスクラップし買い換 65

67 えた場合の優遇税制や補助金の導入が重要である 長期的な政策枠組みの方向性インドの運輸部門には 燃費性能に優れた乗用車を普及させることによる大きな省エネポテンシャルが存在する 将来的に これの実現に資する政策立案ならびに制度の導入が必要である 6. 燃費性能に優れた軽量乗用車 重量乗用車の普及促進 インドが導入を検討している燃費基準は車両重量と CO2 排出量を基にしている このため 軽量で燃費性能に優れる小型車が 大型車に比べて相対的に規制水準が厳しいものになっている 将来的にインドの消費者の選好が大型車にシフトする中で 燃費性能に優れる大型車の普及を進めていくことが重要である 7. 燃料価格政策 関連税制のグリーン化 インドは燃料価格に対する補助金を支出しているが 低廉な燃料価格は運輸部門のエネルギー消費量を増加させる要因となる 国際的な国際価格の上昇による財政負担の増加により 2010 年にガソリンへの補助金の支出が打ち切られた 2014 年には 石油価格の下落を受けてディーゼルへの補助金を打ち切った 一方で 燃料価格に含まれる物品税が急遽引き上げられた インドの消費者は乗用車の維持費用に影響する燃料価格の見通しに非常に敏感であり 購入段階での燃料選択に影響するため 燃料価格の将来の見通しを確保することは非常に重要である 同時に 省エネを進めていくためには 消費者の購入に影響を与える物品税等の税制の長期的なグリーン化の方向性が非常に重要である 66

68 7. 今後の課題 本年の調査結果を踏まえ 以下の点が今後の課題として挙げられる 1. 燃料転換から燃費改善への移行 インドの消費者は燃料価格に非常に敏感であり 価格の変化に対して燃料の転換による対応を行う傾向がある 一方で 燃費性能に優れる乗用車は割高であり 購入段階で敬遠されてしまう 燃費性能の優れた乗用車への移行を促すためのインセンティブが重要であることは BEE へのヒアリングやワークショップでの議論で共有されているが 具体的なインセンティブを付与できる制度が存在していない あるいはインセンティブとして機能させることが困難な状況である 燃料転換ではなく燃費改善による省エネに移行するためにも インド政府及びカウンターパート機関と共同でインセンティブ制度の設計や定量的な分析を示すことが必要である 2. エコドライブなどの省エネ行動を促すための啓発 アンケート調査から 乗用車の利便性を損なうような省エネ行動に消極的であることが明らかとなった 一方で 燃費を改善するための運転方法への高い関心が示された このため インドで乗用車の所有者に対してエコドライブを普及させ 省エネ行動を促すための啓発の枠組みを構築していくことが必要である また 日系メーカーと共同でこうした取組みを進めることで 将来的な燃費性能に優れる乗用車の普及につなげることを検討していく必要がある 3. モーダルシフトの可能性 インド各地で大気汚染や渋滞対策として交通インフラの整備が進められている この 1 つとして 大都市圏を中心にメトロの整備が進んでいる しかし アンケート調査からモーダルシフトの可能性が非常に低いことが示唆された グジャラート周囲以外の地域でも同様であるか 省エネの観点からも継続して調査を進めていく必要がある 4. 重量車の燃費基準策定 インドでは 2014 年 1 月に 2017 年から燃費規制を開始すると発表があった これは乗用車を対象とする物である トラック輸送が急速に拡大しているが 多くが旧型トラックで運行も効率的ではないことが課題となっている 67

69 BEE は乗用車の燃費基準に続いて 重量車の燃費基準についても検討を開始している 既に 日本では重量車のトップランナー制度が導入されており こうした知見をインド側と共有し活用することができると考えられる 68

70 Appendix 1 アンケート質問票 Questionnaire 0 Basic information of the respondents such as: 0.1 Gender Male / Female 0.2 Age years years years years years years and above 0.3 Occupation (choose from below) 1. Private service 2. Govt. service 3. Self-employed (like business, professional, freelancer, etc) 4. Retired 5. Unemployed 6. Housewife 7. Other (specify ) 0.4 Size of household (No of people) 0.5 Household type 1. Joint, 2. Double income with kids 3. Double income without kids 69

71 4. Single income with kids 5. Single income without kids 0.6 Living area (urban, suburban, rural, etc.) 1. Urban 2. Suburban 3. Rural 0.7 Total Monthly Household Income 1. Less than Rs 30, <Rs 30,000-50, <Rs 50, , <Rs 100, , <Rs 200, , More than Rs 500,000 1 Profile of motorized vehicles in household for personal use 1.1 Two wheelers 1. No. of two wheelers in the household 2. On an average the two-wheelers are years old. 1.2 Four wheelers 1. No. of four wheelers in the household 2. On an average the two-wheelers are years old. 3. Details about the four wheelers in the household SN. Manufactu M Seatin Engin Fue Fuel Avg. Purc Date of rer od g e l efficienc Month hase Purcha el capaci capaci typ y (on ly use cost se ty ty (cc) e road) 70

72 Vehicle usage 2.1 Our typical usage of 1 two wheeler in the family is: 1. No. of to & from trips (total) in a week; 2. No. of Kms. per week; a. Up to 25 b. 50 c. 75 d. 100 e. 150 f. 200 g. more 2.2 Our typical usage of 1 four wheeler in the family is: 1. No. of to & from trips (total) in a week; 2. No. of Kms. per week; a. Up to 50 b. 100 c. 250 d. 500 e

73 f g. More 2.3 Our fuel consumption for different types of fuel on weekly basis is: Sr. No more a. Petrol Ltrs b. Diesel Ltrs c. LPG Kgs d. CNG Kgs e. Electricity [No. of recharges] 2.4 Our fuel consumption per month in Rupee terms is: Sr <500 No a. Petrol b. Diesel c. LPG d. CNG e. Electricity more 2.5 Our fuel consumption as a proportion of our monthly household income is: 1. 5% 2. 10% 3. 15% 4. 20% 5. 25% 6. More 72

74 2.6 We plan our monthly fuel budget on a regular basis. Yes / No 2.7 If yes, what is the method you follow to prepare your monthly budget? Explain briefly, 2.8 Do you get your car serviced (inspection/maintenance) periodically? Yes / No 2.9 If yes, how often do you get your car serviced? 1. Once a month 2. Once every three months 3. Once every six months 4. Once a year 5. Once every three years 2.10 By whom do you get your car serviced? 1. I do it myself 2. By my friend 3. Authorized manufacturer service center 4. Local service center 2.11 Our average annual car maintenance cost is: 1. Less than Rs 3,000 73

75 2. <Rs 3,000-5, <Rs 5,000-10, <Rs 10,000-20, <Rs 20,000-50, More than Rs 50,000 3 Factors considered for purchasing a new car 3.1 We have planned to replace or add a new vehicle in near future. Yes/No 3.2 Primary reason for buying a new car; 1. Old car had low mileage 2. High maintenance cost of the old car 3. Old car had aged and had to be replaced 4. Growing needs of the family 5. To meet increasing commute needs 6. For meeting various social needs 7. Other reasons 3.3 We have bought same size and type of vehicles (when replaced or added vehicles) Yes / No 3.4 While buying a vehicle the following parameters are considered by us: 74

76 (Rank 1 for very high importance to 5 least importance) Sr. No a. Price (capital cost) b. Maintenance Cost c. Running cost d. Design e. Engine Power f. Fuel/Engine type e.g. Petrol, diesel, CNG, LPG, Electric g. Vehicle sturdiness h. Manufacturer/brand i. Vehicle weight j. Occupancy k. Manufacturers claims on fuel efficiency l. On-road fuel efficiency m. other customers opinions n. Automobile experts views in media o. My known mechanics opinion p. Special deals/offers q. Track record 3.5 What is the price range in which you are looking to buy this new car? 1. Less than Rs.3 lakhs 2. Rs.3 to 6 lakhs 3. Rs.6 to 10 lakhs 4. Rs.10 to 15 lakhs 5. More than Rs.15 lakhs 75

77 4 If you are planning to purchase a 4 wheeler in the near future? 1. If planning to purchase a petrol, then go to Q no If planning to purchase a diesel, then go to Q no If planning to purchase a CNG, then go to Q no On an average a diesel car costs about Rs. 1 lakh more than the equivalent petrol car variant while petrol prices are about 14% higher than diesel prices.7. If price differential between petrol and diesel were to increase (with petrol becoming more expensive than diesel) and other fuels remaining at the same price difference as of today, then what would be the impact on your choice of car fuel technology under the following situations: a. Petrol prices become 25% higher than diesel prices a. Will still surely choose a petrol car b. Might reconsider the petrol car c. Re-consider buying some other fuel car d. Will surely choose some other fuel car 1. If response is either b, c or d, then what would be the alternate vehicle fuel choice be? a. Diesel b. CNG c. LPG d. Electric 2. If response is either b, c or d, go to Question No. 4.4, else continue. 7 In Gandhi Nagar - Petrol(Rs.67.75/lt) and HSD prices (Rs.59.42/lt) as applicable From Midnight: October, November, , as reported in and on 3rd November,

78 b. Petrol prices become 35% higher than diesel prices a. Will still surely choose a petrol car b. Might reconsider the petrol car c. Re-consider buying some other fuel car d. Will surely choose some other fuel car 3. If response is either b, c or d, then what would be the alternate vehicle fuel choice be? a. Diesel b. CNG c. LPG d. Electric 4. If response is either b, c or d, go to Question No. 4.4, else continue. c. Petrol prices become 50% higher than diesel prices a. Will still surely choose a petrol car b. Might reconsider the petrol car c. Re-consider buying some other fuel car d. Will surely choose some other fuel car 5. If response is either b, c or d, then what would be the alternate vehicle fuel choice be? a. Diesel b. CNG c. LPG d. Electric 77

79 4.2 On an average a diesel car costs about Rs. 1 lakh more than the equivalent petrol car variant while diesel prices are about 14% lower than petrol prices8. If price differential between diesel and petrol were to invert (with diesel becoming more expensive than petrol) and other fuels remaining at the same pr i ce difference as of today, then what would be the impact on your choice of car fuel technology under the following situations: 1. Diesel prices become as much as petrol prices a. Will still surely choose a diesel car b. Might reconsider the diesel car c. Might consider buying some other fuel car d. Will surely choose some other fuel car 2. If response is either b, c or d, then what would be the alternate vehicle fuel choice be? a. Petrol b. CNG c. LPG d. Electric If response is either b, c or d, go to Question No. 4.4, else continue. 3. Diesel prices become 20% more than petrol prices a. Will still surely choose a diesel car b. Might reconsider the diesel car c. Might consider buying some other fuel car d. Will surely choose some other fuel car 8 In Gandhi Nagar - Petrol(Rs.67.75/lt) and HSD prices (Rs.59.42/lt) as applicable From Midnight: October, November, , as reported in and on 3rd November,

80 4. If response is either b, c or d, then what would be the alternate vehicle fuel choice be? a. Petrol b. CNG c. LPG d. Electric If response is either b, c or d, go to Question No. 4.4, else continue. 5. Diesel prices become 50% more than petrol prices a. Will still surely choose a diesel car b. Might reconsider the diesel car c. Might consider buying some other fuel car d. Will surely choose some other fuel car 6. If response is either b, c or d, then what would be the alternate vehicle fuel choice be? a. Petrol b. CNG c. LPG d. Electric If response is either b, c or d, go to Question No. 4.4, else continue. 7. If the same model and car make chosen was made available in a CNG variant and at the same price with CNG made adequately available, would you consider buying it instead? Yes/No e. If no, then why not? Go to Q. no

81 4.3 On an average a CNG car costs about Rs. 50,000 more9 than the equivalent petrol car variant. However, its running cost is almost half that of petrol per kilometer.10if the price of CNG increased with other fuels remaining at the same price difference as of today then what would be the impact on your choice of car fuel technology under the following situations: 1. CNG prices become as much as diesel prices a. Will still surely choose a CNG car b. Might reconsider the CNG car c. Might consider buying some other fuel car d. Will surely choose some other fuel car 2. If response is either b, c or d, then what would be the alternate vehicle fuel choice be? a. Petrol b. Diesel c. LPG d. Electric If response is either b, c or d, go to Question No. 4.4, else continue. 3. CNG prices become as much as petrol prices a. Will still surely choose a diesel car b. Might reconsider the CNG car c. Might consider buying some other fuel car d. Will surely choose some other fuel car 9 Based on average Wagon R prices across different models as on 3 rd November, 2014 from 1_dvlink 10 Petrol versus CNG cost comparisons as available at: on 3rd November,

82 4. If response is either b, c or d, then what would be the alternate vehicle fuel choice be? a. Petrol b. Diesel c. LPG d. Electric 5. CNG prices become 25% more than petrol prices a. Will still surely choose a CNG car b. Might reconsider the CNG car c. Might consider buying some other fuel car d. Will surely choose some other fuel car 6. If response is either b, c or d, then what would be the alternate vehicle fuel choice be? a. Petrol b. Diesel c. LPG d. Electric If response is either b, c or d, go to Question No. 4.4, else continue. Go to Q. no If an electric variant of the same car that you are buying today was made available to you at the same price along with adequate public charging facilities, would you consider buying it instead? Yes/No 1. If not, then why so? 81

83 4.5 In your opinion as compared to petrol/diesel the use of alternative fuels used in vehicles lead to the following: CNG LPG Electric increases transport economy Yes / No Yes / No Yes / No improves vehicle life Yes / No Yes / No Yes / No reduces air pollution Yes / No Yes / No Yes / No reduces noise Yes / No Yes / No Yes / No reduces space in vehicle Yes / No Yes / No Yes / No increases carrying capacity Yes / No Yes / No Yes / No increases pick-up (0-50 kmph) Yes / No Yes / No Yes / No makes road transport very expensive Yes / No Yes / No Yes / No 5. Response to fuel price change 1. When the fuel prices go up we respond in the following manner [Please tick mark suitably.] Sr. Strongl Neutra No Statement y Agree l. Agree a. We reduce our fuel consumption by specific efforts b. we decrease our fuel budget allocation c. we divert budget from other expenses to fuel consumption d. we have switched our fuel type; Petrol to Diesel e. we switched our fuel from Disagr ee Strongl y Disagr ee 82

84 Petrol/Diesel to CNG, LPG, Electric. f. we opt for car / vehicle pooling g. we switched from four wheelers to two wheelers h. we started practicing No Car day & No Two Wheeler Day during the week/month. i. we opted for work from home option j. we reduced from 6 days to 5 days working per week k. we stopped using air conditioner in our car l. we learnt and started conducting efficient driving techniques m. we sold off our two wheeler / car n. we bought a more fuel efficient car o. Any other technique / strategy to balance fuel price hike. 6. Urban transport 1. I use public transport per week 2. I use the following urban transport: i. Bus 83

85 ii. Auto - rickshaw iii. Railway iv. Metro v. Other 3. If the fuel prices go up, would you opt for more utilization of public transport? Yes / No 4. If yes, which urban transport would opt for? i. Bus ii. Auto - rickshaw iii. Railway iv. Metro v. other 84

86 Appendix 2 アンケート結果 Research Report Study to promote energy savings in Indian Transport Sector 1.1 Introduction: Institute of Energy Economics Japan (IEEJ) and School of Petroleum Management (SPM), Pandit Deendayal Petroleum University (PDPU) Gandhinagar collaborated to undertake a joint market research study to understand the choices and behaviors of users of two and four wheel vehicles in the state of Gujarat. This research project is funded through funding by Ministry of Economy, Trade and Industry of the Government of Japan. The prime objective of this market research study is to understand the choices and behavior of users of two wheel and four wheel vehicles so that based on findings and conclusions of the study a set of recommendations could be submitted to the Government of India towards developing a fuel pricing policy which would lead to fuel efficient consumption of fossil fuels and other alternative fuels. 1.2 Rationale for the study: It is forecast that automobile demand in India will continue to increase. This will lead to an increase in fuel consumption over the next few years. With delay in abolishment of fuel subsidy for various reasons the financial burden on national treasury and petroleum companies continues. Fuel economy standards are under consideration by the Government of India but this would lead to increase in the prices of the vehicles compliant with such standards. On the other hand vehicle emission control standards have been introduced to minimize air pollution without being able to create supply of fuel that meets those norms. Thus with increasing demand for petroleum products, subsidy burden delayed, and lack of availability of technology either for low emission fuels or for high efficiency vehicles, it becomes imperative to devise a policy that helps resolve the identified issue and improves energy consumption structure of the country. With this background and rationale the market research study is undertaken. 85

87 1.3 Research Methodology: To understand the choices and behavior of users of two and four wheel vehicles in the state of Gujarat it was decided to undertake an exploratory research study through a well developed data collection instrument. To obtain a state wide understanding and also to obtain responses from large cities and smaller towns, quota sampling is employed. With identified objectives of the research study a questionnaire was jointly developed by team members of the IEEJ and SPM-PDPU. To support the contribution of TERI Delhi, suitable questions were added as per joint discussion between IEEJ and SPM-PDPU. 1.4 Research Objectives: It is important to understand the choices of vehicles, fuels and technologies amongst the users of two wheel and more importantly four wheel vehicles. It is also important to understand factors effecting fuel choices and arguments against particular fuel option. Finally it is important to understand customer response to fuel price changes. Accordingly the following research objectives are listed for the market research study To obtain the demographic profile of users of two and four wheel vehicles Understand vehicles ownership and usage patterns for two and four wheel vehicles Understand future plan for purchase of four wheel vehicles Understand factors considered while deciding on purchase of four wheel vehicle Understand response to fuel price changes across various fuel choices Understand the modal shift behavior in respect of public transport 1.5 Data Collection, Collation and Cleaning: For the identified research objectives data is collected from eight cities and towns across Gujarat State using a well structured pilot tested questionnaire. Professionally trained teams of data collection executives are used for efficient and effective data collection. Data responses are collected from 1100 respondents of which one is not considered for data analysis due to incomplete responses. Collected data was entered in M S Excel software by qualified team of data 86

88 entry operators and was double blind checked for accuracy. Minor entry errors were corrected through physical verification. After correction data was collated for suitable tabulation and cleaning before transporting to SPSS software. Through SPSS software tables for responses are generated for frequency and percentage responses. Due to the nature of questioning not all respondents would respond to all questions and hence valid percentages of responses are calculated as applicable. Appropriate cross tabulated percentages are also drawn from the available data set. 1.6 Analysis and Interpretation: Having developed tables for all question-responses and relevant cross tabulations, charts and graphs the data is subjected to analysis. The process followed is to pick out the salient data points in the form of minimum and maximum values and outlying values for each tabulated data. Data reading is thus undertaken. Data reading leads to interpretation of meaning offered by the data set for us to draw inferences and conclude the possible behavior and choice estimates. 2 Data presentation, reading, inferences and conclusions: The following sections offer data presentation, readings and inferences that help build the conclusions from the data available. 2.1 Respondent Profile: For any study it is important to get responses from the correct sample through suitable sampling design and implementation. The following data presentation helps understand sample profile which decides if the sample is a good representative of the population under study. Table A, Centre-wise Sample Distribution Frequency Percent Valid Percent Cumulative Percent Valid Ahmedabad Anand Bhavnagar Rajkot Baroda Surat Mehsana

89 Bhuj Total Readings Total sample size is 1099 respondents from 8 different cities across Gujarat state. The highest percentage is 18.2% for Ahmedabad & 18.1% for Surat. Rajkot & Baroda have 13.6% & 13.7% respectively. Respondent from all other smaller cities constitute approximately 9% of total sample. Inferences Total sample size for the research, covering 8 cities across the state, with more than 1000 respondents is a good representative sample for the research work. The demography of the respondents matches the prevailing country demographic conditions including both big and small cities. Table B, Two / Four Wheelers Ownership Frequency Percent Valid Percent Cumulative Percent Valid Two Wheeler Four Wheeler Total Readings Of total respondents 30.1% are the owner of two wheeler vehicle. 69.9% respondents are owners of four wheeler vehicle. Inferences Larger representation of four wheeler owners offers better understanding of the four wheel vehicle owners behavior. 88

90 Since four wheel vehicles consume more fuel the impact of the fuel prices is more on the four wheeler owners, hence the sample is taken accordingly. Table 0.0.1, Respondent Gender Frequency Percent Valid Percent Cumulative Percent Valid Male Female Total Missing System 4.4 Total Readings Percentage of male respondents is approximately 82.6%. Percentage of female respondents is approximately 17.4%. Inferences Major respondents are male which is depicting the societal situation of the country. Table 0.0.2, Respondent Age Frequency Percent Valid Percent Cumulative Percent Valid More than Total Missing System 2.2 Total

91 Readings The data is categorized into 6 categories from age group like 18-20, 21-30, 31-40, 41-50, & more than 60 The highest percentage is 47.9% from the age group Respondent from age group are of 24.9%. The percentages from the age group & are 14.3% & 7.2% respectively. Inferences Majority of the respondent are of (21-30) age group with 47.9%. The most of the vehicle owners are in the age group of which consist of 72.9%. The vehicle owners with age more than 60 are very few in numbers. Table 0.0.3, Respondent Occupation Frequency Percent Valid Percent Cumulative Percent Valid Private Service Govt Service Self-employed Retired Unemployed Housewife Others (Student) Total Missing System 6.5 Total Readings 90

92 Majority of the respondents are private employees with a high percentage of 50.4% of total. Total self employed personnel are 29.1% of total. The Housewife and others (which also includes students) are 6.8% & 7.8% respectively. Inferences Half of the vehicle owners are private employees. Another majority section of the vehicle owners are self-employed personnel. Astonishingly govt. employees are not the major vehicle owners with very less percentage of 3.4%. Table 0.0.4, Respondent Household size (No. of people) Frequency Percent Valid Percent Cumulative Percent Valid Total Missing System Total Readings 91

93 33.8% of the respondents have 4 members in the household. Respondents with the family size of 5 & 6 are of 25.3% & 19.9% respectively. Table 0.0.5, Respondent Household size (by category) Frequency Percent Valid Percent Cumulative Percent Valid Total Missing System Total Readings There are 9.9% respondents with the family size of 3 or less than 3 members 60.5% of respondents are having family of 4-5 members. 28.9% of respondents are there with more than 5 members in the household. Common Inferences for Table & Table % of respondents have household size of 4-6 members. 9.2% of respondents have 7 or more members in the family. Very respondents are there with number of households 3 or less than 3. Table 0.0.5, Respondent Household type Valid Cumulati Frequency Percent Percent ve Percent Valid Joint Double Income with Kids Double Income without Kids Single Income with Kids Single Income without Kids Total Missing System

94 Table 0.0.5, Respondent Household type Valid Cumulati Frequency Percent Percent ve Percent Valid Joint Double Income with Kids Double Income without Kids Single Income with Kids Single Income without Kids Total Missing System 4.4 Total Readings Respondent household type is categorized into 5 categories like joint families, double income with and without kids, & single income with & without kids. Maximum respondents are of category single income with kids which is 47.4%. Joint families constitute significantly of 41.4% of total respondents. Inferences Respondents consist majorly of two extreme household types, either from joint families or from single income with kids. Joint families still exist in the country which is significantly showing in sample with 41.2%. Highest percentage is 47.2% of the type single income with kids. The other types of households consist only 11.2% of the total respondents. Table 0.0.6, Respondent Domicile type (urban, sub-urban, rural, etc.) Frequency Percent Valid Percent Cumulative Percent Valid Urban

95 Suburban Rural Total Missing System 8.7 Total Readings Respondent s domicile type is categorized into 3 types, urban, suburban & rural. Urban respondents are 98.9% of total respondents. Suburban & rural category consist only 1.1% of total respondents. Inferences Respondents are majorly from urban area only. Suburban & rural areas are not the significant part of the research. Table 0.0.7, Respondent Total Monthly Household Income Frequency Percent Valid Percent Cumulative Percent Valid Less than 30, ,000-50, ,000-1,00, ,00,000-2,00, Total Missing System 2.2 Total Readings Total monthly income is categorized into 4 categories like less than 30000, , , The income group of consists of 48.3% of total respondents. Respondents with income less than are 42.2% of total respondents. 94

96 Inferences Majority of the respondents for the research are from middle class income group and which consist of 90.5%. Higher income group consist only 9.4% of total respondents. Over all conclusions on respondent profile: From the above data presentation, reading and inferences it is evident that the sample is very representative of the population targeted for the study. The geographic spread and number of responses from different parts of the state covers all geographies. Similarly the sample represents the population on identified demographic variables of income, age, occupation, size and household type and rural-urban domicile. 2.2 Personal use motorized vehicle ownership: It is necessary to understand the current scenario of motorized transport ownership for personal use. Accordingly questions were included in the questionnaire to obtain data on the ownership patterns of two and four wheel vehicles. The following sections provide data reading, interpretation and inferences to conclude the ownership profile of motorized vehicles in the households of Gujarat. Table 1.1.1: Personal use Motorised Vehicle Ownership: No. of Two Wheelers Frequency Percent Valid Percent Cumulative Percent Valid or more Total Missing System 2.2 Total Readings Total number of two wheelers in the household is categorized into 3 categories for this question; 1 two wheeler per household, 2 two wheeler per household, 3 or more two wheeler per household. Household with 2 two wheelers are the highest which is 45.7%. Households with only 1 two wheeler are 42.8% of total respondents. 95

97 Inferences Majority of the household have only 1 or 2 two wheelers in the sample. Households with 3 or more than 3 two wheelers are also significantly 11.6% of total respondents. Table 1.1.2, Average age of Two wheelers in the household: No. of years Frequency Percent Valid Percent Cumulative Percent Valid Total Missing System 7.6 Total Readings Two wheelers which are 3 year old, 4 year old and 5 year old are 24.6%, 23%, & 15.6% of the total sample. Two wheelers which are only 2 year or less than 2 year old are 18.2%. 96

98 Two wheelers more than 5 year old consist of 18.6%. Table 1.1.2a, Average age of Two wheelers in the household: (by category) Frequency Percent Valid Percent Cumulative Percent Valid 2 years or less to More than Total Missing System 7.6 Total Readings Average age of the two wheelers is categorized into 3 categories like 2 or less than 2 year old, from 3-5 year old and more than 5 year old two wheelers. 63.2% of the total two wheelers are 3-5 year old. Two wheelers which are only 2 or less than 2 year old are 18.1% of total Two wheelers with the respondents. Common inferences for Table 1.1.2, Average age of Two wheelers in the household: No. of years & Table 1.1.2a, Average age of Two wheelers in the household: (by category) Majority of the respondents use their two wheelers for only 5 or less than 5 years which is 80.9%. There is also not so high percentage (only 4.2%) of new two wheelers in the survey. Table 1.2.1, Personal use Motorised Vehicle Ownership: No. of Four Wheelers Frequency Percent Valid Percent Cumulative Percent Valid

99 Total Missing System Total Readings 92.9% of the respondents have only 1 four wheeler in the household. Percentage of household with no four wheeler or 2 four wheelers are 3.2% & 3.5% respectively. Inferences Most of the respondents are the owner of 1 four wheeler in their household. Only 3.9% of total respondents have 2 or more four wheelers in their household. Table 1.2.2, Personal use Motorised Vehicle Ownership: No. of years Frequency Percent Valid Percent Cumulative Percent Valid

100 Total Missing System Total Readings Percentage of four wheelers of age 2 years, 3 years, & 4 years are 24.1%, 23.9%, 15.9%. Percentage of new four wheelers which are 1 or less than 1 year old are 12.3%. Four wheelers of age 10 years or more than 10 years is very low of 3%. Table a, Average age of Four wheelers: (by category) Frequency Percent Valid Percent Cumulative Percent Valid 2 or less to or more Total Missing System Total Readings Average age of four wheelers is categorized into 3 categories like 2 or less than 2 years, 3-5 years, & 6 or more years. Majority of the four wheelers are of age from 0-5 years which is 83.8%. 16.3% of the four wheelers are of age 6 years or more than 6 years. Common inferences for Table 1.2.2, Personal use Motorized Vehicle Ownership: No. 99

101 of years & Table a, Average age of Four wheelers: (by category) Significant percentages (i.e. 36.6%) of respondents have new four wheelers which are 2 year old or less than 2 year old. Almost half of the total four wheelers are of age between 3-5 years. Respondents do not use very old four wheelers which are 10 or more than 10 year old. Overall conclusions on personal use motorized vehicle ownership: With about 30% respondents as owners of two wheelers on an average one to two two-wheelers are owned in a typical household. Most two wheelers are not more than 6 years old with almost 50 % being up to three years old. Average age of two wheelers can be considered up to 3.5/4 years with most vehicles going off the roads by the 7 th year. Most households own only one four wheeler per household. Most four wheelers are less than 5 years old with most vehicles going off the roads by the 7 th year. 2.3 Personal use motorized vehicle usage: To estimate typical usage pattern of owners of two and four wheel vehicles questions were included to collect data for the same. The data in form of number of trips per week and number of kilometers travelled per week is obtained. To estimate fuel usage, data is collected for average weekly consumption in volume and value terms for different fuels. Funding habits are estimates by collecting data on fuel consumption as percentage of monthly household income and budgeting habits. Further it is necessary to evaluate habits of vehicle maintenance and servicing. The following section presents the vehicle usage and fuel consumption related information. Table Number of to and from trips per week: Two Wheelers Frequency Table Cumulative Frequency Percent Valid Percent Percent Valid

102

103 Total Missing System Total Readings There are 1099 respondents from which 1087 have responded suitably and data of 12 respondents is incomplete. There is highest frequency of 169(15.4%) amongst 20 to & from total trips in week. The following values of number of to & from trips have shown minimum 102

104 frequency of 1:- 0, 1, 4, 11, 21, 27, 38, 42 and 50. Total percent of frequency of 1 is 0.9%. Table Number of to and from trips per week: Two Wheelers (Categorised) 2 Wheeler - No of to & from trips in a week in category Cumulative Frequency Percent Valid Percent Percent Valid 15 or less to or more Total Missing System Total Readings Data is divided into three categories with number of to and from trips per week being 15 or less, 16 to 25 and 26 or more. There are 1099 respondents from which 1087 have responded suitably and data of 12 respondents is incomplete. Maximum frequency of 576(52.4%) can be seen in the category of 16 to 25. Minimum frequency of 240(21.8%) can be seen in the category of 15 or less. Inferences Most of the population has 16 to 25 numbers of trips per week. Table Number of Kilometres travelled per week: Two Wheelers 103

105 Cumulative Frequency Percent Valid Percent Percent Valid Up to More than Total Missing System 4.4 Total Readings There are 1099 respondents from which 1095 have responded suitably and data of 4 respondents is incomplete. There is a maximum frequency of 271 for those who have travelled 100 kilometres per week. There is a minimum frequency of 4 for those who have travelled 25 and below kilometres per week. Inferences 271(24.7%) respondents, which are maximum, travel 100 kilometres per week. 104

106 There are only 4(0.4%) respondents who travel 25 and below kilometres per week. Table Number of to & from trips per week: Four Wheelers Cumulative Frequency Percent Valid Percent Percent Valid

107

108 Total Missing System Total Readings There are 1099 respondents from which 746 have responded suitably and data of 353 respondents is incomplete. There is maximum frequency of 120 for 10 to and from trips per week. There is minimum frequency of 1 for the following values of number of to and from trips per week: - 9, 13, 17, 36, 38, 45, 50, 55, 60, 84, 91, 100 and 105. Table Number of to & from trips per week: Four Wheelers (Categorised) Cumulative Frequency Percent Valid Percent Percent Valid 10 or less to or more Total

109 Missing System Total Readings There are 1099 respondents from which 746 have responded suitably and data of 353 respondents is incomplete. Data is divided into three categories: 10 or less, 11 to 20 and 21 or more to and from trips per week. Maximum frequency of 335 is therefore the category of 11 to 20 to and from trips per week. Minimum frequency of 88 is there for the category of 21 or more to and from trips per week. Inferences Most number of respondents have between 11 to 20 to and from trips per week. Only few respondents have 21 or more to and from trips per week. Table Number of Kilometres travelled per week: Four Wheelers Cumulative Frequency Percent Valid Percent Percent Valid Up to

110 More than Total Missing System Total Readings There are 1099 respondents from which 750 have responded suitably and data of 349 respondents are incomplete. Maximum frequency of 377 is there for 100 kilometres travelled per week. Minimum frequency of 1 is there for travel per week of 1000 or more kilometres. Inferences Most of the respondents are those who travel 100 kilometres per week. Respondent who travels 1000 or more kilometres per week are rare. Table 2.3A Weekly fuel consumption: Petrol in litres Cumulative Frequency Percent Valid Percent Percent Valid Less than

111 More than Total Missing System 4.4 Total Readings The data is divided into the followings even categories: less than 5, 6 to 15, 16 to 25, 26 to 40, 41 to 50, 51 to 100 and more than % respondents have 5 and less litres of weekly petrol consumption. 41.1% respondents have 6 to 15 litres of weekly petrol consumption. Inferences Maximum proportion of respondents has 5 and less litres of weekly petrol consumption. Minimum respondents are in the category of weekly fuel consumption between 41 to 100 litres of petrol. Table 2.3B Weekly fuel consumption: Diesel in litres Cumulative Frequency Percent Valid Percent Percent Valid Less than